In this article we would like to explain Insights Global’s tank terminal commercial performance model and why this model offers essential insights into tank storage demand drivers.

Introducing Insights Global’s Conceptual Model

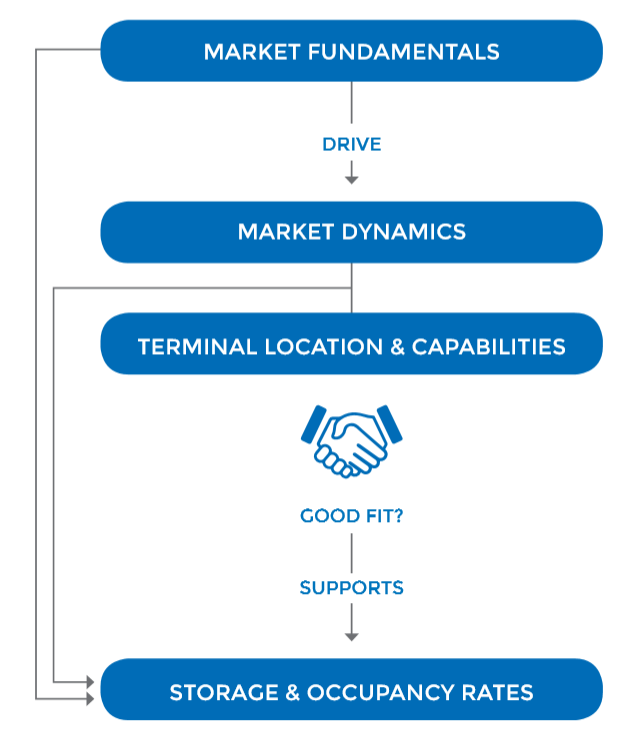

Insights Global’s tank terminal commercial performance model (see figure: 1) shows the relation between a terminal’s market environment and its commercial performance. The environment is divided into market fundamentals (which have a slow rate of change) and market dynamics (which have a fast rate of change).

In our model the fundamentals drive dynamics. A terminal that has a good fit with market dynamics will find storage rates are being better supported. Besides market dynamics also market fundamentals influence storage rates.

Learn what drives tank storage demand. Join the FREE Webinar: Insights Global Tank Terminal Commercial Performance Model upcoming March 18th 2020.

Detailed graphical representation of ‘Market Fundamentals’ and ‘Market dynamics’ as part of Insights Global’s conceptual model Tank Terminal Commercial Performance

Market fundamentals are:

- The shape of the forward curve;

- The competitive structure; and

- Logistical factors such as supply, demand, imbalances and trade flows.

Market dynamics are:

- Inventory levels;

- Arbitrage and trade flows;

- Changes in product spec; and

- Variation in vessel sizes.

These variables have a direct impact on a terminal’s operations and on a terminal’s requirements. When a terminal is able to react faster to these dynamics in relation to its competition, it is more likely that it can create superior commercial performance.

Do you want to understand the essential insights into tank storage demand drivers?

In order to explain the essentials of the model we would like to invite you to join our webinar, presided by Insights Global’s Managing Director Patrick Kulsen.

Key highlights of webinar are:

- Impact of the forward curve on a terminal’s commercial performance

- Impact of S&D and imbalances on a terminal’s commercial performance

- Impact of arbitrage and trade flows on a terminal’s commercial performance

- Explanation of how trading companies make money

Learn what drives tank storage demand. Join the FREE Webinar: Insights Global Tank Terminal Commercial Performance Model upcoming March 18th 2020.

Insights Global’s Tank Terminal Week Report has been based on these essential parametrics that drive tank storage demand. This report will improve your understanding of the world of oil trading and as a result offers you the chance to make intelligent decisions.