25 July, 2019 (Argus) — Inventories of oil products independently held in Amsterdam-Rotterdam-Antwerp (ARA) fell this week from two-year highs a week earlier.

Overall stocks fell in fuel oil inventories. Suezmaxes left the ARA area for west Africa and to Singapore, where a bunker fuel shortage has opened the arbitrage from Europe after two months of limited flows.

Naphtha inventories fell to the lowest level since January 2017. Seaborne arrivals fell and demand held firm both locally and along the Rhine river. Demand from gasoline blenders has been supported in recent weeks by high transatlantic outflows of gasoline. Tankers carrying naphtha arrived in the ARA area from Denmark, Portugal, Russia and the UK.

Outflows of gasoline to the US fell on the week, but transatlantic

shipments remained at a high level with a rise in tankers departing for Latin

America. A week-on-week increase in gasoline cargoes arriving from Russia

supported inventories, which rose by 1.1pc. Tankers also arrived from France,

Norway and the UK. Barge congestion eased in Amsterdam.

Gasoil inventories rose by to a nine-month high. Demand from along the Rhine ticked down for a second consecutive week. With almost no rainfall forecast in the southwest of Germany until the end of July, German importers spent the early part of summer preparing for possible low Rhine water levels by moving gasoil barges from ARA up the river for inland storage. Falling Rhine water levels have since prompted the imposition of barge loading restrictions and subdued the trade.

ARA jet fuel stocks fell to a seven-week low. Demand was firm, seasonally. A part-cargo arrived from India, and tankers departed for the UK.

The tank storage industry is a very competitive market and it brings many challenges to its players. Tank terminal operators for liquid bulk are facing both internal and external factors that can affect the efficiency and the progress of their business.

A few internal factors involve the company’s organization, processes, availability and infrastructure, etc. Terminal operators can be also challenged by external factors, such as competition, regulations and the economy. With more than 7,040 tank storage facilities worldwide, it can be very tough for storage operators to position themselves in the market.

What exactly do terminal operators need to know in order to face their competition?

1 Location

Location for terminal operators is key for the success of their business. Before starting with any terminal construction project, a lot of thought is put into the geographical location of the terminal. In order to analyze the location, a storage operating company needs to have insights on all other players that are active in that area. Besides other factors, analyzing the competition in a certain area can indicate if it is viable to invest in a project.

If a terminal operator already has an existing terminal in a certain region, it is important to know the neighboring competition. Who are those terminal operators? What is their market share? What cargo types do they support? What is the infrastructure of those terminals? All these are a few crucial questions, that terminal operators should ask themselves.

2 Market share and total storage capacity

Another important factor for a terminal operator is to know the largest storage players in the region. This gives the ability for a terminal operator to analyze his/her position in the market and at the same time understand the power of their competition.

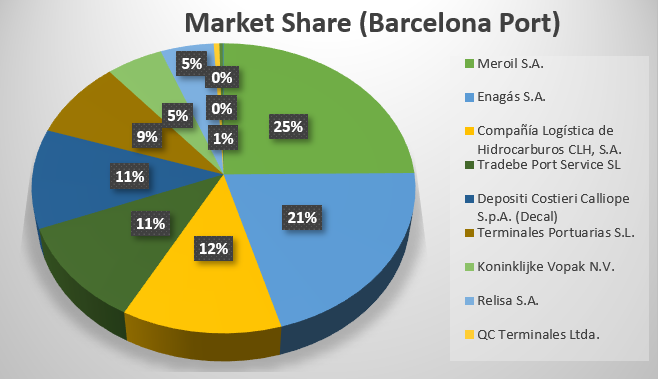

How can they easily determine the market share of their competitors? For example, if a terminal operator is interested in Barcelona Port or has an existing terminal in the port, they can look at the total storage capacity of all the terminal operators. In the image below it can be seen how insightful market share is when identifying the biggest players in the port (the market share is drawn from the total capacity of each terminal in the port).

3 Cargo types

For terminal operators it is important to know what cargo types their competitors are able to store. This gives an opportunity for them to create diversity and flexibility in product storage at their terminal. In today’s storage industry, the clients of storage operators see diversity and flexibility as an added value. Thus, there are a few important factors that a terminal operator needs to analyze:

Demand in that region

Production in that region

Import and export flows

Imbalances

Storage availability in that region

4 Different terminal functions and access modes

A tank terminal can have the following functions:

Strategic storage

Logistical storage

Import/Export

Trading hub

These four different terminal functions create different level of competition for terminal operators. Tank terminals that are located in the same trading hub and that are providing the same storage services are in direct competition. A strategic storage that is located next to a logistical storage might not be in direct competition, but terminal operators should still thoroughly analyze the level of competition.

The function of a terminal can also dictate the access modes for a terminal. Terminals can have the following access modes: sea, rail, road, pipeline and barge. A terminal with more access modes can be connected with different international trading markets and provides more options and flexibility for its potential clients.

5 Planned investments and expansions

Terminal operators need to know if there are any new projects or planned expansions in their region. A new terminal can mean stronger competition while a new expansion creates more power to an existing competitor. If terminal operators are aware of the new changes and are properly informed, they can better understand how to face the new challenges.

As the competition is significantly increasing, especially in port areas, terminal operators need to constantly evaluate their infrastructure system and consider expansion possibilities.

What should a terminal operator know about a new project/expansion:

Which company is it and what is their market share?

What will be the total added capacity for an expansion or what will be the total capacity of the new terminal?

When will the project be completed?

What products will the terminal be able to store?

What access modes will the terminal have?

6 Logistical performance

A very important factor for marine terminal operators is to analyze the logistical performance of their competition. This includes the following operations:

Throughput

Berth occupancy

Average visit duration

Tank turns

What does the logistical performance measure?

It determines the productivity and performance of a certain terminal. For a terminal operator, it is a good indicator if the competition is underperforming.

Conclusion:

The six factors mentioned in this article are very good indicators and analysis tools that a terminal operator can use in order to determine the efficiency of its terminal. And also to create a plan in order to improve the market share of the terminal. Nevertheless, besides these six factors there are many other factors that can help to evaluate the competition and were not mentioned in this article.

If you are a terminal operator have you thought about these factors?

19 July, 2019 (Bloomberg) – ARA stockpiles of diesel and gasoil increased to their highest level in a month as an emerging contango in ICE gasoil futures for the next few months offered an incentive to some market players to store, according to Insights Global. * Gasoil/diesel stockpiles, the highest since mid-June and highest for the time of year since 2016 ** Stockpiles also grew on higher imports from Russia, Saudi Arabia and the U.S. in past week, Lars Van Wageningen of Insights Global said by phone ** MIDEAST-EUROPE FUEL FLOWS: July Volumes Set to Mark Another Gain * Jet fuel stockpiles, highest for the time of year in data starting from 2007 ** Stockpiles increased on higher imports from other regions, including larger LR2 shipments from India and Singapore; higher volumes arriving in Europe to serve seasonally strong jet fuel demand: Van Wageningen ** Exports to the U.S. were lower in the past week while inflows to ARA increased from elsewhere in NW Europe, Russia and Spain; those volumes are likely destined for future exports: Van Wagenigen ** Higher Baltic imports in past week including cargoes from Lithuania, Poland and Russia outweighed exports to West Africa and the Middle East, Van Wageningen said, adding that the arbitrage opportunity to Asia is currently closed

19 July, 2019 (Argus) Inventories of oil products independently held in the Amsterdam-Rotterdam-Antwerp (ARA) area have risen in the past week to reach their highest level since May 2017.

Stocks of all

surveyed products except naphtha increased, with gasoline inventories rising

the most in percentage terms. Tankers loaded with gasoline arrived in ARA from

France, Norway, Russia, Spain and the UK in the past week, with inflows from

the Mediterranean and Russia notably high. The arbitrage route from northwest

Europe to the US remains open and market participants are bringing gasoline and

blending components to the region ready for transatlantic export. Tankers left

the region for the US, Argentina, the Caribbean and the Mediterranean. The high

volume of incoming and outgoing seaborne cargoes added to the congestion in the

gasoline barge market, particularly around Amsterdam. Tankers and barges often

load and discharge from the same jetties.

Gasoil inventories rose in the past week to reach their highest level since October 2018. Demand along the river Rhine ticked downwards after inland restocking pulled in high volumes during the previous week, and seaborne arrivals from Russia rose. Tankers also arrived from Saudi Arabia and the US, while cargoes left for France, the UK and west Africa.

Fuel oil stocks rose. No tankers departed for key arbitrage destination Singapore, but fuel oil cargoes did depart for the Mediterranean, Saudi Arabia and west Africa. Tankers arrived from Lithuania, Poland and Russia.

Jet fuel stocks in the ARA area rose during the past week. Demand from the aviation sector was firm in line with seasonal expectations, and market participants suggested that there was little spot volume available. Tankers arrived from India and Singapore, and departed for Denmark, Ireland and the UK.

Naphtha inventories bucked the trend, falling on the week amid firm demand from gasoline blenders in the ARA area. Tankers arrived from Algeria, Denmark, France, the Mediterranean, Russia and the UK, while none departed.

12 July, 2019 (Argus) – Inventories of oil products independently held in Amsterdam-Rotterdam-Antwerp (ARA) fell in the week to today.

Stocks of all surveyed products except naphtha fell on the week. Fuel oil inventories fell most heavily, dropping -week lows. The very large crude carrier (VLCC) Cosdignity Lake departed Rotterdam carrying oil cargo and a smaller tanker departed for west Africa. The arbitrage route to Singapore appeared to be workable in the past week. Vitol booked the VLCCs Front Duchess and FPMC C Melody to take fuel oil to Singapore, loading in Rotterdam on 15 July and 2 August, respectively.

Gasoil inventories fell. Demand from along the river Rhine was steady on the week with gasoil heading inland on barges. Disruption to refining activity caused by the Druzhba pipeline outage in April-May weighed on inland inventories, which are now being restocked. Tankers arrived from Russia and the US and departed for France and the UK.

Gasoline inventories fell on the week. Tankers arrived in ARA from the Black Sea, Norway, Russia, Spain and the UK. But higher demand from the US and rising demand from west Africa supported outflows. Gasoline barges continued to suffer loading delays in the Amsterdam area, with barges and tankers competing for slots.

Jet fuel stocks in ARA fell. Demand from the aviation sector was firm in line with seasonal expectations. No jet fuel tankers arrived in ARA during the reporting period, but at least one departed for the UK.

Naphtha inventories climbed on the week, with rising prices drawing in cargoes from Algeria, France, Latvia, Spain and the UK. The return from scheduled maintenance of several petrochemical facilities in Europe and firm demand from the gasoline blending sector has supported naphtha prices in northwest Europe and bolstered inflows.

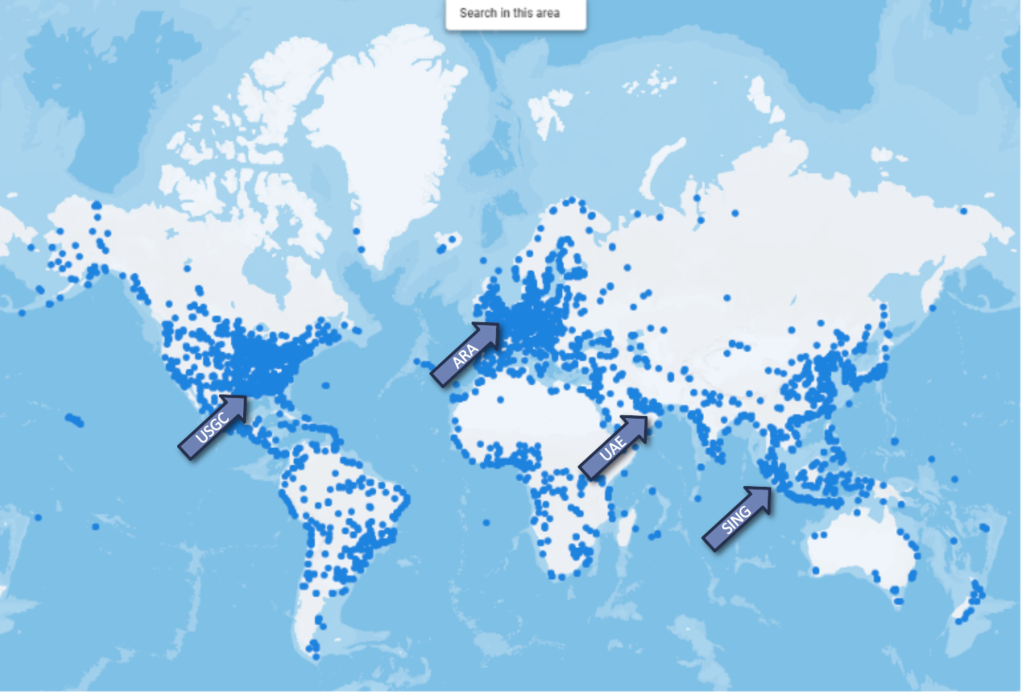

The oil and gas storage market is approximately 1.30 billion cubic meters in size and it is estimated to grow as more than 70 new projects and expansions are set to be completed till 2022¹. There are approximately 5000 tank terminals worldwide that offer their storage space for third party leases. These terminals are located all over the world and in some regions, they form clusters with large storage capacities. The four major storage hubs are located in Antwerp-Rotterdam-Amsterdam, Singapore, Fujairah and Houston.

The oil trading business is extremely competitive and trading companies are focusing on providing high level services. Major trading companies are investing in logistics and infrastructure in order to satisfy their customers and have advantage over their competitors.

What are the most essential factors that traders are looking for when assessing a storage opportunity?

1. Location and function

For trading companies it is important to have an overview on the location of terminals across the world and the operators of these terminals. Traders should be able to break down the terminal storage market according to the location and function. Tank terminals have different classes depending on their purpose. There are strategic, logistical, import/export terminals and trading hub terminals. Traders are interested in terminals that offer them the possibility of using their assets for trading activities. F.e. the blending services provided in Amsterdam offer gasoline traders the possiblity to blend the product to a country’s spec and move it to WAF or US.

2. Reliability

It is becoming very common that there are a lot of fake companies that claim to be real tank farms and are usually claiming to be located in major trading hubs. It can be difficult to distinguish real tank terminals from the fake ones, as some scammers are building websites almost identical to those of real terminal operators. Trading companies should be able to have access to trustworthy data that informs them about real tank farms in order to prevent scams.

See here a lits of websites that are claming to be real tank farms in Rotterdam.

3. Contacts

Key contacts are very important for any company in order to build a strong network and to drive business success. However, due to many privacy laws it is increasingly become very difficult to find key contacts, especially in the tank storage industry.

After trading companies have done their research and defined a strategic focus on certain terminals, they need to find contact details of those terminals. With these contacts, mainly the commercial manager of the operator, conditions of a tank storage agreement can be negotiated.

4. Flexibility

Multimodal terminals can optimize and facilitate the transportation or products, but it can also minimize costs for trading companies. Terminals have sea, barge, rail and pipeline access that move products into different parts of the world. More access modes offer trading companies more flexibility. For example, if barge freight rates go up due to low Rhine water levels, trading companies can switch to rail delivery.

Truck: Delivering products with a truck offers the possibility to reach complex terrains.

Rail: Rail access can be low cost and offers fast delivery.

Pipeline: Fixed pipelines might be costly to build but for a long term these offers continuous supply.

Barge: Using barge transportation on certain rivers can be low cost and offer connection to local markets.

Sea: Sea access offers connection to international markets and different ships in size and purpose can be used.

5. Tank and cargo types

When analyzing suitable terminals trading companies can also analyze the tank types that a terminal holds. As oil products require different storage needs, tanks can vary in their design, shape, material and equipment. Different tanks can suggest the products that certain terminal stores thus indicating if the terminal is suitable for a trader’s needs. Moreover, it is important to have information on the cargo types that a terminal can store. Even though tank types can give a good indication on the products that the terminal can hold, it is not always accurate, as some tanks can hold more than one product type.

Conclusion

For trading companies to successfully lock in profits of an oil trading deal, some supply chain analysis is required. A trader seeks full flexibility and optionality to cash in opportunities. Finding a fitting storage is therefore of upmost importance. The factors that play a curcial role in this storage assesment are: location, reliability, contacts, flexibility and tank & cargo types.

¹ TankTerminals.com

The data for this article was gathered with the support of TankTerminals.com database platform. With only a few clicks and couple of seconds the information of the biggest market players in the various regions was obtained.

By Greta Talmaci

If you have any questions, please email me at: gtalmaci@insights-global.com.

Read here about “The hottest terminal locations of 2020”

8 July, 2019 (Bloomberg) – ARA stockpiles of gasoline drew in the past week on elevated transatlantic shipments of the road fuel, according to Insights Global. * Gasoline stockpiles fell in the week to July 3; that was the biggest one-week draw since mid-May ** The arbitrage opportunity on the route re-opened after U.S. gasoline prices jumped in the aftermath of the fire and explosion at the PES refinery, Lars van Wageningen, operations manager at Insights Global, said by phone ** EUROPE-AMERICAS FLOWS: PES Fire Prompts Surge in Loadings

** Stockpiles drew after Suezmax Minerva Evropi loaded fuel oil and departed for Singapore; exports to Mediterranean, West Africa also played a part: Van Wageningen * Gasoil/diesel stockpiles, the highest since mid-June and above average for the time-of-year ** Stockpiles gained mainly as a result of elevated imports from India as well as inflows from Russia and the U.S., outweighing the impact of stable flows inland along Rhine: Van Wageningen * Click here for summary of latest weekly changes; see full dataset

4 July, 2019 (Argus) – Inventories of oil products independently held in Amsterdam-Rotterdam-Antwerp (ARA) have increased by in the week to 3 July, buoyed by a rise in gasoil stocks, according to consultancy Insights Global.

Gasoil inventories rose. Production of middle distillates in the region is rising as refineries in northwest Europe return from planned or unplanned outages. These include three German facilities — Schwedt, Leuna refinery and Vohburg refineries — as well as the Rotterdam refinery and Cressier plant.

Gasoline inventories fell on the week as a result of higher exports to the US Atlantic coast and Canada. An increase in gasoline blending activity caused barge congestion in Amsterdam and Rotterdam as market participants moved finished grade product and components around the area. Tankers departed ARA area for Brazil, west Africa and northern Germany. But increasing refining activity in Germany is likely to curtail gasoline tanker movements from ARA to the country. Gasoline cargoes arrived from the Baltics, Finland, Norway, Spain and the UK.

Naphtha inventories rose on the week, after falling by a similar amount the previous week. Rising northwest European naphtha prices attracted cargoes from Algeria, Norway, Portugal, Russia and the UK.

Fuel oil inventories fell on the week. Tankers departed for the Mediterranean, west Africa and the Suezmax Minerva Evropi left Rotterdam for Singapore. Cargoes arrived in the ARA from France, Lithuania, Russia and the UK.

Jet fuel stocks in ARA fell back slightly from the two-year highs recorded during the last three weeks. Demand rose in line with seasonal expectations. But the return to service of the Leuna refinery weighed on demand for jet fuel barges on the river Rhine, as supply from inland increased. Jet fuel tankers arrived from the UAE and departed for the UK and Ireland.

As of

September 1st 2019 René Loozen will join the INSIGHTS GLOBAL team to

take the role of Consultancy Business Director. In this role he has the

assignment to shape, grow and lead the global consultancy organization in order

to bring more value to INSIGHT’s clients. His extensive background in the hydrocarbon,

chemical, shipping and tank storage industry, his exceptional ability to

understand markets and his solid experience in shaping business intelligence

organizations makes him the ideal person to lead this effort.

Patrick Kulsen, Managing Director of INSIGHTS GLOBAL, who previously held this role, will remain available as a senior consultant for clients and will intensively work together with René to maximize value for INSIGHTS’ clients and other stakeholders.

Patrick: ‘René’s

expertise in the chemical supply chain really supplements our knowledge base. It’s

perfectly in line with our corporate strategy to focus more on rising

intelligence demand in the chemicals market.’

René: ‘Insight Global’s data driven

andquantitative approach combined

with an excellent knowledge of the oil and chemical value chain really helps to

facilitate INSIGHT’s customers to make commercial decisions’

ABOUT

INSIGHTS GLOBAL:

INSIGHTS

GLOBAL an independent market research company specialized in international

petroleum and petrochemical industries. We offer market data, market analysis

reports, consultancy and training services to our customers to support their

commercial decision making.

27 June, 2019 (Argus) — Inventories of oil products independently held in the Amsterdam-Rotterdam-Antwerp (ARA) area have risen this week, boosted by gasoline and fuel oil stock builds.

Total oil product stocks in the ARA hub rose in the week to 26 June, according to consultancy Insights Global. The week-on-week increase was driven by rises in fuel oil and gasoline inventories, respectively (see table).

Gasoline refining margins in Europe rose this week, boosted by increased demand for the product as a result of the shutdown of Philadelphia Energy Solutions Philadelphia. Sellers are likely accumulating gasoline in tanks ready for blending before export to the US in the coming weeks.

Rising prices drew in cargoes from Italy, France, Portugal and the UK.

Gasoline barge movements rose on the week as market participants organised

product for export. But demand from along the Rhine fell on the week.

Refineries affected by the Druzhba crude pipeline contamination gradually

returned to full production.

Fuel oil inventories rose on the week. Exports were limited with inventories in key market Singapore ample. No VLCCs loaded during the week to yesterday.

Naphtha supplies held in ARA storage fell during the past week. An oversupplied naphtha market in the last month has weighed on prices and inhibited shipments to northwest Europe. No tankers came from key supply areas north Africa and Russia.

Gasoil inventories fell. German demand rose, prompting a week-on-week increase in middle distillate barge traffic on the Rhine.

Jet fuel stocks in ARA fell back slightly from the two-year highs recorded during the last two weeks. High inventories in northwest Europe prompted several jet fuel tankers from the Mideast Gulf to divert to the US and Africa, weighing on shipments to the ARA area. Demand from along the Rhine continued to rise as consumption increased in line with seasonal expectations.

Reporter: Thomas Warner

GDPR Consent

Our website uses cookies. Click on the 'Accept all' button to accept the cookies and on the 'Settings' button for more information and settings.