(Bloomberg) — Stockpiles of gasoline in independent storage in Amsterdam-Rotterdam-Antwerp in the past week fell to the lowest since August as the Russia oil-contamination crisis drained inland supply of the motor fuel, according to Insights Global. * Gasoline stockpiles – week to Thursday, lowest for time of year since 2015 ** The Russia oil contamination issue is affecting inland supply by hampering operations of some refineries, Lars van Wageningen, operations manager of Insights Global, says by phone; says ARA inventories are falling as more gasoline moves up the Rhine to replace missing volumes and inland oil product terminals look to replenish their supplies ** Export flows to the U.S. have also increased in the past week, and shipments to West Africa are also still “quite hefty”: Van Wageningen * * Fuel oil stockpiles, highest since Jan. 24; moves back above 5-year seasonal avg ** Inventories gained on stockbuilding for future arbitrage shipments, Van Wageningen says, adding that while arb economics to Singapore were unfavorable in past week they look to be improving ** VLCC ADS Serenade is in Rotterdam, tanker-tracking data compiled by Bloomberg show; the tanker is due to load fuel oil in coming weeks: Van Wageningen

London, 16 May (Argus) — Weaker gasoil and fuel oil demand led a rise in

overall oil product stocks held independently in the

Amsterdam-Rotterdam-Antwerp (ARA) region, and offset a decline in remaining

product inventories, including gasoline.

Russian crude imports through the Druzhba pipeline to Germany were stopped on 25 April because of a contamination problem. The issue led to a draw in independent gasoline stocks in the ARA region after regional blenders looked to fill supply shorts in inland Europe, particularly Germany and Poland. A rare shipment took a gasoline cargo to a north German port from the ARA storage hub, according to consultancy Insights Global. Inland flows are typically carried by barge, or in the opposite direction for stock building. Shipments of gasoline from the Mediterranean region to northwest Europe have also surged in recent weeks following the pipeline issue.

Stronger prompt gasoline prices in northwest Europe have diminished arbitrage opportunities out of the region, while steep backwardation in the gasoline market is encouraging volumes to move out of storage. Supply is likely to tighten further as a technical issue yesterday forced the closure of Total’s Leuna refinery in southeastern Germany. The firm declared force majeure on rail deliveries of oil products from the facility.

This adds to the unplanned shutdown of Total’s Grandpuits and a turnaround at the firm’s Donges refineries. One of the two crude distillation units (CDUs) at BP’s Rotterdam refinery in the Netherlands, is also under maintenance.

Reduced diesel exports from Primorsk in May, following a decrease in

scheduled loadings and bankruptcy proceedings at the Antipinsky refinery, have

tightened the northwest European market. But the impact of the Druzhba pipeline

issue on the diesel market has been less pronounced, largely as a result of

relatively higher inventories and lower demand compared with gasoline. Gasoil

stocks rose following arrivals from Russia, the US and Latvia, while product

was exported to Argentina, Ireland, UK and west Africa.

Naphtha stocks in the ARA region fell from four-week highs the previous

week, on steady demand and reduced incentive to bring product into the storage

hub. Buying interest for open-specification product has come under downward

pressure from unusually high levels of scheduled maintenance in the

petrochemical sector. But demand for blending grades was supported by firm

gasoline demand from inland destinations.

Jet fuel inventories remained steady in the week to 16 May on limited

demand, as most imports from east of Suez arrived into UK and French ports. In

addition, estimated arrivals into northwest Europe this month have declined to

1.5mn t, from 2mn t previously, following diversions to African destinations.

Weaker arbitrage economics to take fuel oil to the Asia-Pacific region from northwest Europe supported stock levels. Inventories in Singapore reached over a two-year high of in the week to 10 May. Despite unviable export economics, Gunvor chartered a very large crude carrier (VLCC) to load fuel oil in Rotterdam to Singapore.

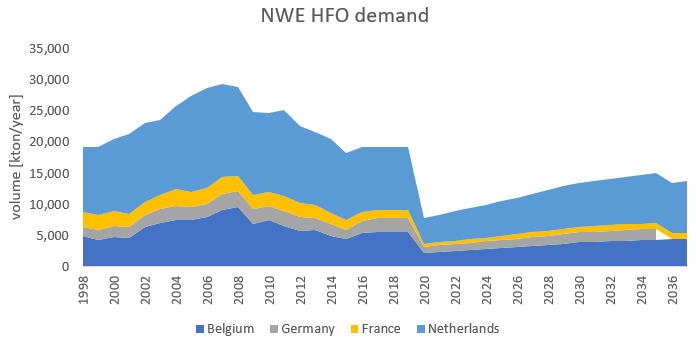

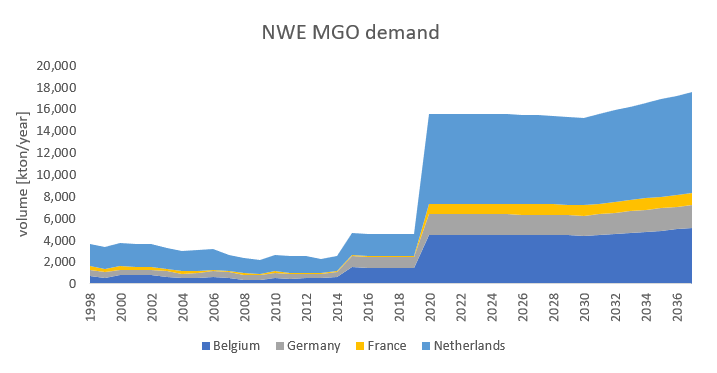

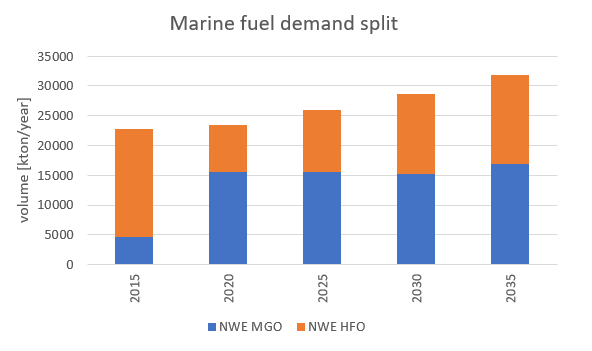

Insights Global structurally forecasts the future supply and demand of oil products in the ARA region and naturally incorporates IMO 2020 into its models. In our forecasting models we predict an annual growth rate for marine fuels that is adjusted for efficiency gains of ships, while the split between HSFO and MGO in bunker demand switches in 2020 and is submissive to price changes and upcoming alternative fuels. We predict a sharp decline in heavy fuel oil demand with simultaneously a jump in the demand for (marine) gasoil in 2020. The heavy fuel oil demand is expected to more than half in size, whereas MGO demand is predicted to quadruple. Our assumption for the post-2020 era is that the shipping industry will gradually switch back to fuel oil using scrubbers or 0.5% LSFO. Furthermore, LNG will take in a more dominant position, up to 11% in 2030. This will diminish the share of gasoil used and lead to a slight decline in gasoil demand between 2020 and 2030.

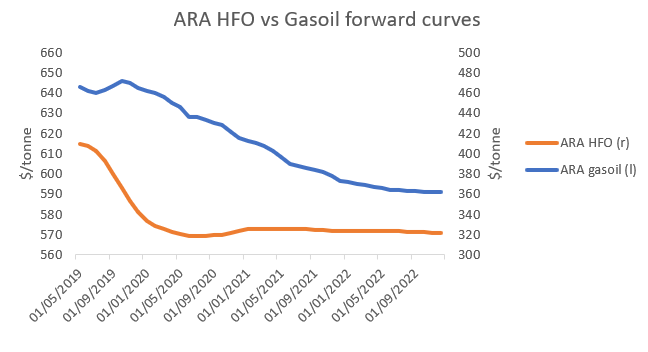

The transition from high sulphur fuel oil to marine gasoil and the changing demands for both products can be seen in the futures markets. The forward curve for HFO makes a steep dive towards the beginning of 2020 when the regulation comes into force. The gasoil prices show an inverted pattern: a small contango until the start of 2020 can be seen as demand for the product will be the largest when the legislation becomes active. After these initial price extremities of gasoil and HFO the markets settle down as HFO prices recover slightly while gasoil prices enter a backwardated situation. This is in line with our demand forecasts and resembles the extent to which alternatives such as scrubbers gain an increasingly larger share. We expect subsequent waves of investments in shipping but also in refining, as the production of 0.5% fuel oil becomes more profitable. For more complex refineries with a certain crude slate this will offer opportunities while for other, more simply configured refineries, their continuity is at stake.

A Change for

the Tank Storage Business

The ARA region currently is a

net-importer of gasoil and is the final destination for many of the world’s

gasoil flows. Estimates are that in 2022 the deficit would increase by between

+12% and +34% relative to 2018 values, primarily driven by IMO 2020. The changing imbalances of gasoil

and fuel oil in the ARA region will have an impact on the ARA tank storage

business. The lower fuel oil demand will increase the oversupply of fuel oil in

the region and as such affect all tank terminals who lend their facility to

this product. The

changing environment for fuel oil tank storage will eventually lead to higher fuel

oil storage rates in the region. Fuel oil storage rates are likely to remain depressed in

2019, but when the IMO regulation hits the markets in 2020 the oversupply of fuel oil is likely

to switch the markets into a contango, supporting the storage business. This

effect is expected to be reinforced when the crude markets switch to contango

as well.

Higher storage rates for fuel oil

are thus expected, but the current fuel oil tank storage business nevertheless faces

a tough time from a logistical point of view. Terminals in ARA specialized in fuel oil are

either busy in the bunkering market or in the transit business. In the first

case these terminals will suffer from the reduced size of the HFO bunker

market. In the second case the business is more related to the flow from Russia

towards Far-East. This transit flow is also expected to be marginalized in the

medium term and long term. Therefore tank terminal operators storing HFO will

need to anticipate on these changes and explore options in order to cope with

possible oversupply of fuel oil tanks. Less tanks for fuel oil storage will be

needed, but opportunities lie in diversification. From 2020 onwards more grades

of bunker fuel (a.o. ULSFO, 0.5% LSFO, 3.5% HSFO) will need to be stored, while

smaller tanks as well as blending capabilities will become more important.

Running up to the bunker fuel spec

change in 2020 the fundamentals for the gasoil storage market are likely to

improve following more interest in middle distillate tanks and the need for

more grades of gasoil. The contango that is developing in the gasoil markets

supports the storage rates as well. In 2020 however we expect a halt to the

growth of gasoil storage rates caused by a backwardated market structure

following the higher spot prices. After 2020 we expect storage rates to improve

with the gasoil markets following the contango formation in the crude markets,

albeit to a smaller extent. More tanks are needed in this bunker market to

store middle distillates which could increase competition, but occupancy rates

in the medium term will remain high due to increased demand.

(Bloomberg) — Stockpiles of gasoline in independent storage in Amsterdam-Rotterdam-Antwerp fall to the lowest for time of year since 2015, according to Insights Global. * Gasoline stockpiles – lowest since Aug. 30 ** The past week has seen a lot of exports to West Africa, as well as more shipments to the U.S., Lars Van Wageningen, operations manager of Insights Global, says by phone ** Increased flows of gasoline also seen to inland markets by barge along the Rhine: Van Wageningen ** READ (May 7): U.S. Gasoline Imports From Europe Rise to 8- Month High: Customs * Gasoil/diesel stockpiles – lowest since March 21, remain slightly above 5-yr seasonal avg ** More volumes shipped inland via barge along Rhine while weekly imports of diesel from Russia’s Primorsk, Ust-Luga ports declined: Van Wageningen * Naphtha stockpiles highest since March 28 ** Inventories rose in past week due to higher imports from Algeria Reporter: Bill Lehane

In 2020 the international marine bunker fuel markets are in for a big change. For environmental concerns the International Maritime Organization will implement a new policy that limits the sulphur content of fuels burnt in maritime traffic. High sulphur fuel oil has been historically the most widely used fuel for maritime transport, but will most likely lose this position to low sulphur fuels such as marine gasoil or LSFO when the new regulation comes into force. This article dives deeper into the subject, and shares our vision on how the ARA bunkering market and international oil markets will change under the new policy.

As of January 1st 2020 the International Maritime Organization (IMO) requires all marine fuels to have a sulphur content of at most 0.5% of the total mass, down from the current maximum allowed 3.5%. With the exception of a few areas that already have special IMO requirements in place, the new IMO standard will hold globally. Traditionally the bunker fuel market has been a sink for refiners to unload their high sulphur refining resids into. In 2018 an average of seven million barrels of such heavy resids were produced every day, half of which was absorbed by ship bunkers. But the global refining system is not yet equipped to produce such quantities of fuel oil at a sulphur level of 0.5%. The impact of this new regulation is therefore big as most vessels will have to abandon their current fuel oil consumption, therewith completely changing the market dynamics for existing marine fuels and creating opportunities for alternatives.

An important decision for shipowners

The shipping industry faces an important decision for their fuel use under the IMO 2020 regulation, and several options exist for shipowners who need to replace their HSFO consumption.

The most likely scenario is that the majority of the shipping industry switches to using marine gasoil (MGO), which doesn’t require any technical modifications nor upfront investments.

Second, the shipping industry could switch to a new 0.5% low sulphur fuel oil (LSFO) grade. Current global LSFO production capacity is however insufficient to cover a transition from HSFO to LSFO in the bunkering industry, and this change would need vast refinery investments.

The third option is to install scrubbers on board of ships and continue to burn HSFO while the exhaust gasses are being filtered. This is an expensive and lengthy investment for the shipowner, as installation costs range between 2-3 million per vessel and the delivery time to install the scrubber will have the vessel out of operation for a long time.

The fourth option is that the shipping industry switches to burning LNG. Significant investments and concerns about the availability of LNG as a bunker fuel however challenge the implementation.

The fifth option is that the shipping industry switches to methanol. Methanol has a low energy density however and in addition requires a multi-million investment. Given the ease of the transition to marine gasoil compared to the other products the market will initially shift its bunker demand by using marine gasoil when the new regulation goes into effect.

The

increasing of information stream due to digitalization and accessibility to

information sources, has led to numerous debates in the oil markets. Refiners,

traders, brokers, end-consumers and all other stakeholders within the industry

need to cope with decision making on various levels and are therefore relying

on certain proved sources in an industry which is full of closed doors and

limited availability of information. Transparency in this market is therefore crucial

to search and select the appropriate partners within the market and to make

smarter business decisions.

Market

transparency can be found in all different subjects within the oil and gas

industry. Price setting agencies, transport and tank storage rates overviews and

other statistical insights contribute to a level playing field, which can help

the customer make the best decision possible. By obtaining instantly accurate

information, one can reduce mainly costs, time

and effort. Objective players in the oil and gas environment, help balance the

markets by supplying vast amounts of data and information to all participants. Traders

interpret the macro-economic data of NGOs, governmental institutions and

central banks to weight their decisions and therefore depend on reliable

information. Falsified or incorrect information can give individuals an edge

and increases the costs involved for the other businesses.

Moreover, these objective market participants withhold fraudulent companies or individuals from entering and disbalancing the market. Associations such as, FERM Rotterdam (ferm-rotterdam.nl) provide insights over the fake suppliers of tank storage capacity, in order to limit the risks involved for other market participants. Individuals without proper knowledge of the markets, can easily become targets of these scams. Who is able to spot the differences when certain, legitimately looking, websites come across?

Websites about the same terminal in the port of Rotterdam, which one is legitimate?

For

businesses entering the market, these organizations are key to a fruitful

collaboration between suppliers and clients. In addition, these organizations

show which websites, companies or individuals to bypass. Companies and

terminals in the TankTerminals.com database are investigated by various

database administrators before being added in the vast database of terminal

details, characteristics, contacts and other relevant information. Data

supplied by the terminals and the managers of the terminals is thoroughly

checked before it is approved. The data is regularly updated and if possible

expanded with more data to give a transparent overview on the tank terminals.

This way, potential suppliers, customers and others interested have a quick

go-to list which reduces the efforts of going through all kind of information. The

completer the information in the terminal factsheets, the higher the

reliability, legitimacy and opportunities to connect with the relevant

contacts.

Market

transparency is imperative in getting quickly the right information and with as

little errors as possible. The oil and gas industry and its environment has

been closed and constrained. However, it is rapidly changing in the digital age

with the help of different organizations. The information, statistics and other

relevant news can be supplied to the interested individuals and companies in

order to get more insights, to make quicker and smarter decisions.

(Bloomberg) — Stockpiles of gasoline in independent storage in Amsterdam-Rotterdam-Antwerp slumped to the lowest in five months as high exports continued to be seen to U.S. and Latin America, according to Insights Global. * Gasoline stockpiles – in the week to Thursday, lowest since Nov. 15 ** While exports to U.S., Latin America remained elevated over past week, the arbitrage window is now less favorable, potentially meaning lower exports in coming week, Lars Van Wageningen, operations manager of Insights Global, says by phone ** Still, with some spring refinery maintenance still ongoing in Europe as well as unplanned outages — such as at Germany’s Shell Godorf last weekend — higher local demand may limit recovery for stockpiles: Van Wageningen * Gasoil/diesel stockpiles – remains above seasonal avg ** Steady flows inland along Rhine, as well as exports to places like Argentina, outweighed the impact of continuing imports from Russia, U.S.: Van Wageningen * Fuel oil stockpiles remains lowest for time of year since 2014 ** The arbitrage to Singapore has closed again, leading to some restocking: Van Wageningen * Jet fuel stockpiles, highest since May 2017 ** Seasonal demand is not so strong yet, causing a lag in drawdown of stockpiles amid the continuing arrival of imports: Van Wageningen

Argus – Oil product stocks held in independent storage tanks in the Amsterdam-Rotterdam-Antwerp (ARA) trading hub were stable on the week, with increasing fuel oil inventories offsetting declines in gasoil and gasoline.

Fuel oil inventories rose. Fuel oil inventories in Singapore reached 9-week highs on 18 April, inhibiting fresh eastbound bookings from the ARA area. But the VLCC Ridgebury Utik departed Rotterdam on 22 April for Singapore, having partially loaded during the prior week.

Stocks of Gasoil fell slightly this week on steady inland diesel demand, with gasoil booked on Rhine barges. Rising diesel prices and an anticipated seasonal fall in Rhine water levels prompted stockbuilding inland, putting downward pressure on ARA inventories.

Gasoline inventories fell because of higher transatlantic shipments. Tankers departed for the US, Nigeria, Brazil and Latin America. Demand for gasoline barges within the ARA area remained firm, but congestion in Amsterdam and Antwerp delayed gasoline component movements.

Naphtha stocks fell, with gasoline blenders the primary source of local demand. Planned maintenance at petrochemical sites in northwest Europe started to weigh on prices.

Jet fuel stocks reached their highest level in almost two years, buoyed by preparations for higher summer demand. Little movement was reported in the jet fuel barge market, with a single tanker booked to discharge along the Rhine.

Oil product stocks held in independent storage tanks in the Amsterdam-Rotterdam-Antwerp (ARA) trading hub fell in the week to 11 April, with gasoline the only product to record a stockbuild.

Naphtha stocks saw the largest decline in percentage terms, with independent inventories reaching 11-week lows, data from consultancy PJK show. Vessels carrying naphtha offloaded in the ARA region from Algeria and other northern and eastern European ports, and cargo was exported to Asia-Pacific. Inland demand rose, as German firm BASF’s petrochemical facility in Ludwigshafen drew barges.

Strong blending demand for naphtha, coupled with firm Eurobob oxy gasoline barge liquidity on fob ARA barges, may have contributed to a regional gasoline stockbuild ahead of loading dates. Eurobob oxy gasoline barges changed hands on 1-5 April for loading in the trading hub 2-8 days ahead, compared with the prior week period. This may have offset high export levels as arbitrage economics remain viable on gasoline routes to the US, Mexico and Mideast Gulf, where refinery maintenance is drawing additional cargoes. Exports to the US were lower than expected, but are likely to pick up as US gasoline inventories fell last week by their largest weekly volume in more than a year, according to the EIA.

A fall in scheduled exports of low-sulphur diesel from Russia’s Baltic port of Primorsk resulted in lower gasoil stocks held independently in the ARA region. Furthermore, mild weather supported diesel demand for driving inland, with buying interest rising from France and Switzerland.

No jet fuel vessels arrived in the ARA region from east of Suez or the US in the week to 11 April, while a cargo was exported to the UK. At least one vessel carrying jet fuel was scheduled to arrive in Amsterdam on 9 April but has not yet offloaded. And demand along the Rhine was strong ahead of the peak-summer flying season, with PJK recording the largest weekly outflow by barge since June.

But jet fuel stocks on a four-week rolling average basis remained at their highest since the end of November. And levels are expected to rise further. Jet fuel imports to northwest Europe from east of Suez and the US are set to reach this month — similar to March levels. Demand is expected to remain thin, with off-peak buying interest in April more than March levels. Demand in May is only expected to rise from April.

Fuel oil arrivals to the ARA region originated from France, Lithuania, Poland, Russia and the UK. Eastbound flows continue despite weaker economics, with the Koch-chartered Suezmax Nordic Mistral departing Rotterdam for Singapore. And exports to the Mideast Gulf continued for summer power generation.

Welcome to

“GRIPPING THOUGHTS”, the space created by Insights Global where Clients,

Partners and Friends are invited to share ideas and insights that help shedding

light on the challenges that the Oil & Gas industry faces in the near and

long future.

So join us, read and get inspired by our talk to Mr. Koen Algoet – Product Manager Terminal Solutions – and Mr. Kevin Pluvier – Project Manager Oil & Gas – at Agidens, a solutions provider with a workforce of over 600 people that for more than 70 years has been helping companies in various sectors to improve their operations in the areas of security, reliability, efficiency and sustainability.

Q: How would you describe the main market challenges at the present time?

In our

view, the tank terminal market presents two main challenges.

The first

is linked to Operational Excellence. Due to backwardation and the new capacity

added in recent years, it is correct to expect a surplus of storage capacity

that will increase the competition even more and leave profits under stress.

In this environment, there will be a high demand for improved, more efficient processes to guarantee full usage of the existing assets. A good example of how this can be realized is Agidens’ Axcel® smart slot booking solution. Due to increasingly bad traffic conditions, it is very common that trucks don’t make their schedules leaving terminals with empty slots and the necessity to reserve ‘late arrivals’ slots which reduce the normal asset capacity. Axcel® doesn’t use and thus ‘waste’ these empty slots but relies on the smart engine to recalculate updated planning scenarios keeping all available assets and resources into account.

The second challenge is linked to Human Resources. Nowadays there is a high workforce turnover in the industry, as a result of several reasons, among them the fact that young people don’t want to stay in the same job and activity for a long time anymore. The time and energy that is needed to train new employees into working with these manual procedures could be invested in automation. Furthermore, in order to attract and retain young people we can assume that automated terminals will have preference to manually operated terminals as an employer.

Q: And how do you see the industry evolving in a period of 5 to 10 years? What are the main challenges ahead of us?

As it was

said before, due to the high competitiveness of the market there will be a

growing pressure on the terminals in terms of operational excellence, but also

to cope with the speed of innovation.

Even though

there is a lot of interest in Artificial Intelligence, the focus in the next

years will be on Big Data and in learning how to transform what is generated

and collected by sensors – as a consequence of the development of the IoT –

into knowledge.

Agidens

understands the necessity to foster the development of specialists that can

handle this new scenario that encompasses themes as cyber security, GDPR, new

standards and regulations, and questions on how to communicate data between all

the different networks, how to set up this data and how to do it in a secure,

safe and controlled way.

Agidens

embraces the proposition of sitting with the client to understand his problems

and ‘pains’ in a consultative approach. So that the people involved in the

project can take over and develop the product based solutions keeping a vision

of the future time and not only the present.

At last, it is important to mention that no matter how much of a terminal’s management moves to the cloud, all that is related to safety must remain local.

Q: How is Agidens getting prepared for these future challenges?

Agidens

understands that innovation is essential to offer competitive solutions to its

clients, therefore we give special attention to this theme and how to

accelerate its pace. We believe that if we expect to be ready for the

challenges of the next ten years we must act today. First, by keeping a close

relationship between our R&D department and universities as Leuven, Antwerp

and Ghent. Second, by creating a culture and atmosphere that encourages our

employees from different areas to voice their ideas and by granting time,

budget and guidance from R&D for them to be developed.

As an

example, at Agidens as soon as young engineers are hired they have the

opportunity to be in direct contact with clients, especially with people who

work on the field and experience the day to day challenges.

Agidens’ Atalk® solution is an excellent example of a product that was proposed by one of these young talents. While on the field, he noticed that there was a dangerous gap between the moment that a potentially dangerous event started – a fire, for instance – and the moment this information was passed to the personnel at the terminal. So he proposed a system that translates the usual text messages installed upon an existing operational control system such as SCADA or DCS into speech, in a way that now they can be transmitted by voice directly to the walkie talkies of all the employees around the terminal.

At last, it

is important to give people time, support and a lot of training to be able to

cope with the transformation speed of the industry.

PS: if you want to contribute to “Gripping Thoughts” please send an email to acavalcanti@insights-global.com

Find here other “Gripping Thoughts” articles:

Read now the interview with Bertrand Chupin, VP of the Loading Systems business unit of TechnipFMC, a global leader in subsea, onshore/offshore and surface projects, with about 37,000 employees.

GDPR Consent

Our website uses cookies. Click on the 'Accept all' button to accept the cookies and on the 'Settings' button for more information and settings.