As the world is slowly emerging from the Covid-19 pandemic, it is safe to say that the corona virus has had a profound impact on nearly every aspect of our daily lives. Besides the more visible effects on public health, society, and transportation, Covid-19 also sent a shockwave through the global economy.

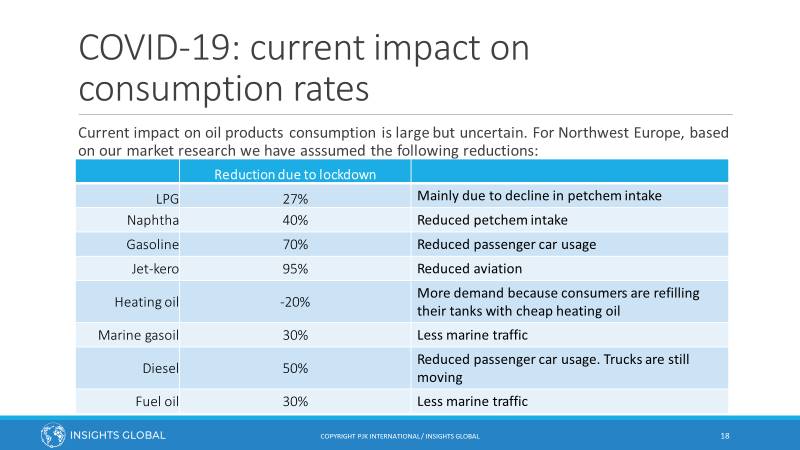

This shockwave also had its effects on tank terminals: As soon as the true scope of the Covid-19 pandemic became apparent, the oil market shifted from a backwardated market into a deep contango. Needless to say, this contango immediately led to a significant increase in demand for tank storage.

The road less traveled?

The demand for road and jet fuels has been affected most by the Covid-19 pandemic. While the short-term effects of national lockdowns on demand for fuels are relatively straightforward (fuel consumption is strongly linked with people’s mobility patterns), it will be the longer-term effects that are the most interesting to keep an eye on.

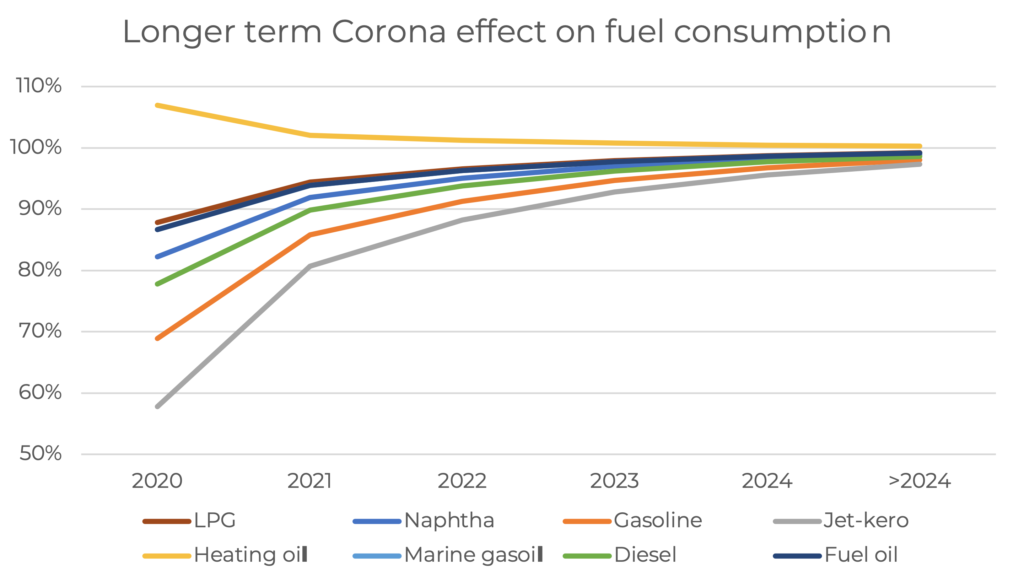

Large corporations like banks, IT companies, and insurers are already preparing for a ‘new normal,’ where their staff will work more from home after Covid-19 than they did before (source). As people will commute less to their offices, a decline in overall car traffic volume could be expected. Together with the ongoing electrification of road vehicles, we expect that the current surplus for gasoline will increase further.

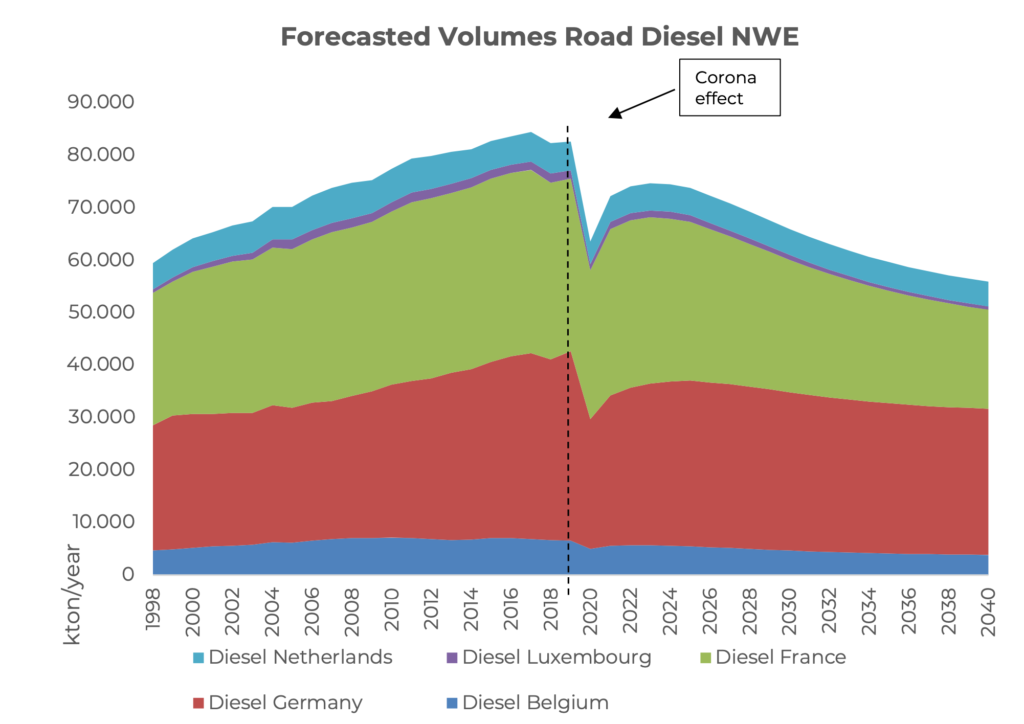

When we take a look at diesel consumption, reversed dieselization of passenger cars will lead to a faster decline than we will see for gasoline. That being said, because the electrification of trucks is not expected to happen in the coming years, there will still be a large volume of diesel consumption left.

For jet fuel, we forecast that the current deficit for North-Western Europe will grow at a slower pace. While it is expected air travel will largely recover, analysts forecast it will take at least towards 2023 until air travel is back at pre-pandemic levels (source).

Electric vehicles

Over the past few years, the market for electric mobility has seen incredible growth. In 2019, the global electric car fleet exceeded 7.2 million, up 2 million from the previous year. With more and more electric car models being introduced to the market and charging infrastructure improving, this strong growth is only expected to increase. The IEA estimates that by 2030, there will be over 250 million electric vehicles (excluding three/two-wheelers) on the world’s roads. According to the IEA, the projected growth in the Sustainable Development Scenario of electric vehicles would cut oil products by 4.2 million barrels/day. (source)

While battery electric vehicles (BEVs) are considered the preferred solution for short-distance and light vehicles (passenger cars, delivery vans) because of their high energy efficiency, their batteries have a limited energy density compared to traditional fuels. This means that for vehicles with high power demands, such as ocean liners, long-haul trucks, and airplanes, batteries are highly impractical.

Alternative fuels

With an energy density that’s comparable to fossil fuels, e-fuels and green hydrogen are poised to play a crucial role in our transition to sustainable mobility. E-fuels are produced by electrolyzing water, creating hydrogen and oxygen. While hydrogen gas in itself is an excellent renewable energy carrier, it can be synthesized further with carbon dioxide or nitrogen into more stable and easier to handle e-fuels. When using electricity from renewable sources and circular carbon dioxide (such as direct capture from the air), net emissions are close to zero.

While this process’s overall energy efficiency is lower than that of chemical batteries used in BEVs, the much higher energy density of e-fuels makes them much better suited for applications with high power demands, like shipping, trucking, and aviation.

Circular economy

As the call for reducing plastic waste gets louder and louder, the concept of circular economy is gaining traction. While the market for recycled plastics is growing rapidly and will have its effect on the demand for chemicals, it is not foreseen yet that consumption of virgin material will decrease the coming years.

What’s next?

It is clear that both the covid-19 pandemic as well as the transition to sustainable fuel sources will greatly impact the tank storage terminals. The market outlook for the oil and chemical industry will see significant shifts in supply and demand, while the Covid-19 pandemic only adds further complexities to the market. That’s why market intelligence should be on the radar of every terminal operator. During our regular Market Update webinars, we offer our expert outlook on supply, demand, and trade flows and their impact on tank storage demand.

Do you want to make sure that you never miss out on important market updates? Sign up for the next webinar today, so that you are better prepared for what tomorrow will bring.