Even though the Covid-19 pandemic is still in full swing, it is safe to say that the corona-virus has had a profound impact on nearly every aspect of our daily lives. Besides the more visible effects on public health, society, and transportation, Covid-19 also sent a shockwave through the global economy.

Even though the Covid-19 pandemic is still in full swing, it is safe to say that the corona-virus has had a profound impact on nearly every aspect of our daily lives. Besides the more visible effects on public health, society, and transportation, Covid-19 also sent a shockwave through the global economy.

This economic shockwave also had its effects on tank terminals: As soon as the true scope of the Covid-19 pandemic became apparent, the oil market shifted from a backwardated market into a deep contango. Needless to say, this contango immediately led to a significant increase in demand for tank storage. Currently, the commercial occupancy rates at oil tank terminals are very high, and as a result, tank storage rates have increased by 20-30%.

This presents a somewhat unique situation for the tank terminal market. On the one hand, high occupancy rates and increased tank storage rates have a very positive impact on the short-term profitability of oil terminals. However, the consumption of oil products has seen a sharp decline and will takes years to recover fully.

What will this mean for the tank terminal market? At Insights Global, we continuously calibrate our Advanced Tank Terminal Market Model against shifts in the market. Our algorithms take into account macroeconomic trends like oil prices, taxes, trade costs, and interest costs, and (petro)chemical factors like trade flows, logistics, and storage rates. Based on the latest economic developments, we have also incorporated the Corona effect in our forecasting models.

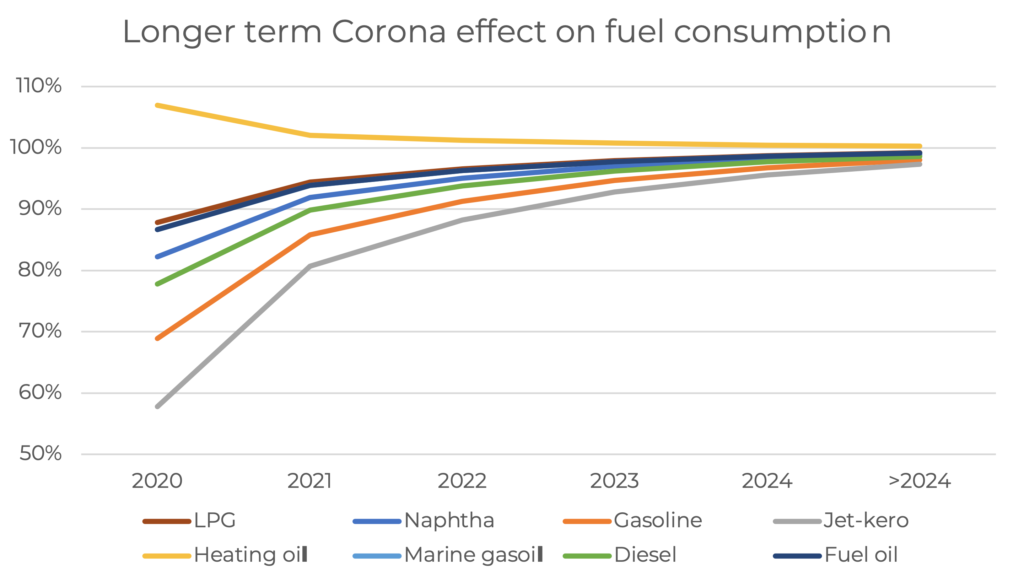

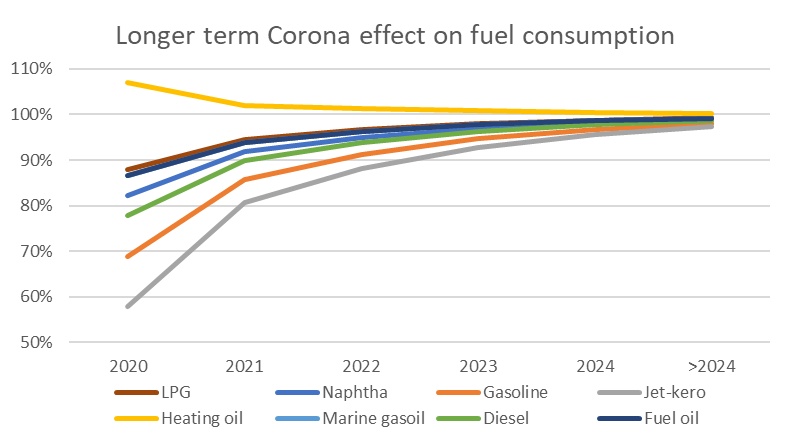

Even though the V-shaped consumption curve (sharp decline followed by a sharp increase) for oil products seems already behind us, we expect it will take five years for consumption levels to normalize fully. Jet-kero consumption is hit especially hard by the Corona-crisis, with an initial reduction of up to 95%. This slow recovery is not only caused by the impending economic recession, but also by the change of habits like working from home and replacing in-person meeting by online meetings.

While the current focus is – understandingly so – on the impact of Covid-19 on the oil market, other essential factors like the electrification of road transport, reverse dieselization of European passenger cars, and IMO 2020 regulation for bunker fuels will also play a key role in the tank terminal market. Naturally, the impact of these events is also incorporated in our Advanced Tank Terminal Market Model.

Having access to accurate, up-to-date oil storage rates is crucial to make the right business decisions.

With our Global Oil Storage Rate Report, you’ll gain access to the single and only authoritative source of storage rate information available worldwide. It will provide you with transparency on price levels in global tank storage markets regularly, so you are always in the know and can set the right ask and bid prices for your storage.

Download your FREE Sample Report now and discover what information you could have at your fingertips each quarter.

Patrick Kulsen and René Loozen of Insights Global consider the impact of COVID-19 and IMO 2020 on bunker fuel consumption and ARA tank storage demand.

The assumption is that the current lockdown lasts three months and has a negative impact on marine fuel bunker consumption levels. After the lockdown, the consumption level will gradually normalise, which will take five years.

The real impact of COVID on global and regional GDPs is not clear yet, but we may conclude that the IMO 2020 regulation have had a positive impact on the ARA tank storage demand.

As we are now well into the second quarter of 2020 it is useful to look back on the introduction of the recent IMO legislation on the regulation of sulphur emissions from bunker fuels. The dust has settled with respect to the implementation of these new rules. But as this happened a ‘black swan’ arrived on the global oil scene: COVID-19 or the Coronavirus. This pandemic and the international crisis it evoked is gripping international trade and impacting on shipping and bunker sales like nothing we have ever seen before. So, this article will also look forward to estimating the medium-term impact on bunker markets and, in particular, on bunker storage markets.

Run-up to 2020

The International Maritime Organization’s (IMO) regulation mandating a reduction in the sulphur content of marine fuels to 0.50% or below came into effect on 1 January 2020.

Leading up to the start of this new era in marine fuels there were multiple opinions or scenarios about which bunker fuels would become dominant. In first instance, most stakeholders thought high sulphur fuel oil (HSFO) would remain a dominant bunker fuel because of the expected uptake of scrubbers. Other stakeholders assumed that marine gasoil (MGO) would become main bunker fuel as there wouldn’t be enough supply of 0.50% very low sulphur fuel oil (VLSFO). Some oil majors, the International Energy Administration (IEA) and consultants then changed their opinions, believing that VLSFO would become the dominant fuel. There were other stakeholders, like the gasoil traders, who thought that the demand for MGO would increase significantly because of IMO 2020.

The first months of 2020

The first months of 2020 have shown that VLSFO seems to be the dominant bunker fuel. Consumption of MGO increased only slightly by around +10%. HSFO accounts for about 20% of total fuel oil consumption, with the rest being mostly VLSFO.

The introduction of the new VLSFOs has led to some compatibility concerns. VLSFO blends can come from residual components and distillate components. Residual components are mostly aromatic due to the asphaltenes in the bottom of the barrel. Distillates are high on paraffins. Blending these two streams together can lead to compatibility issues. This can occur if a ship switches between different batches and the fuel is mixed in the ship’s fuel tank, a process also known as commingling. The co-mingling of bunker fuels from different origins could lead to serious damage to engines or the clogging of fuel lines. VLSFO residue blends, being more aromatic, and hydrotreated vacuum gasoil (VGO), being less aromatic have these compatibility issues.

These compatibility issues also have an impact on the demand for storage capacity as some product owners have taken steps to avoid commingling new fuels in their tanks. So, this calls for segregated tanks, which will increase demand for tanks.

An important and lucrative business for oil traders in the Amsterdam-Rotterdam-Antwerp (ARA) region used to be the transhipment of fuel oil from Russia to the Far East. However, this transit flow has largely disappeared. On the one hand, the supply of Russian fuel oil has gone down whereas the demand for fuel oil in Asia has also dropped significantly. Furthermore, Asian bunker demand for fuel oil is currently being supplied from other closer regional sources. Nowadays, Russian exports are being directly exported in smaller tankers, with the US as the main destination. The ARA is no longer the heavy fuel oil transhipment hub.

Looking ahead

Our assumption in the post-2020 era is that the shipping industry will keep on using fuel oil as the dominant marine fuel (80%) but it is unclear is what the respective shares of VLSFO and HSFO will be.

In our forecasting models, the Corona effect is incorporated. The assumption is that the current lockdown lasts three months and has a negative impact on marine fuel bunker consumption levels. After the lockdown, the consumption level will gradually normalise, which will take five years. Our assumption of five years is based on experience in the past and the enormous fall of GDP which influences the consumption of fuel oil. The International Monetary Fund (IMF) forecasts a 3% contraction of global GDP in 2020, while the Eurozone will see a decline of 7.5% in 2020. It will take several years of GDP growth to be back at the same GDP level as in 2019. The consumption of bunker fuel is heavily correlated with global trade, so we expect it will take several years before bunker fuel market is at the same level as in 2019.

Due to growing bunker fuel consumption and declining average production, surplus in NW Europe will change into a deficit. Terminals in ARA specialising in fuel oil will benefit from the growing size of the fuel oil bunker market. As the number of grades has increased and more components are needed to blend into VLSFO / HSFO / MGO, more storage capacity is needed.

Additionally, on top of these structural effects on fuel oil supply, demand and imbalances, there is an enormous oversupply in the market due to the COVID-19 crisis. This has resulted in a steep contango in fuel oil forward prices and is stimulating traders to buy and store excess fuel oil supply. This provides major support for fuel oil storage rates in the short to medium term.

So, in summary, the introduction of the IMO 2020 regulation and the COVID-19 crisis have had the following impact: • More tanks needed to segregate and blend fuel grades • Less arbitrage flows limit the demand for large tanks • Long term bunker demand growth and rising imbalances will support tank demand • Short to medium term support of fuel oil storage rates due to steep contango.

The real impact of COVID on global and regional GDPs is not clear yet, but we may conclude that the IMO 2020 regulation have had a positive impact on the ARA tank storage demand. Also, in the short to medium term, the COVID-19 / Corona crisis has had a positive effect on the tank terminal business.

The tank terminal market in ARA is facing several challenges and issues that influence the short- and mid-term dynamics. Oil market developments, globally and regionally, could have an impact on the ARA Oil tank terminal market.

We have selected three main themes that impact ARA oil Tank Terminal markets in the short and medium term:

COVID-19 outbreak: Increase in tank demand and storage fees due to massive oversupply on petroleum markets (deep contango)

IMO 2020 and changed bunker fuel specifications: Growing ARA tank storage demand

Electrification of passenger cars: Downward effect on road fuels consumption but mixed effects on tank storage demand

Reverse dieselization of European passenger car sales: The change in car sales might decrease structural imbalances and lead to less demand for tank capacity

COVID-19 outbreak

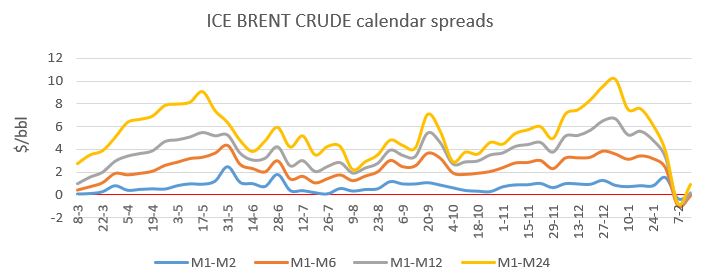

Since the beginning of the Corona crisis the market is clearly in contango. Looking to the calendar spread it was already expected that market would move into contango on a short term. However, the Corona crisis was the big trigger for the start of the contango period. As the graph shows the market is in a deep contango and how long this situation will persist is the main question. It depends on how fast the production and demand of oil products will become in balance again.

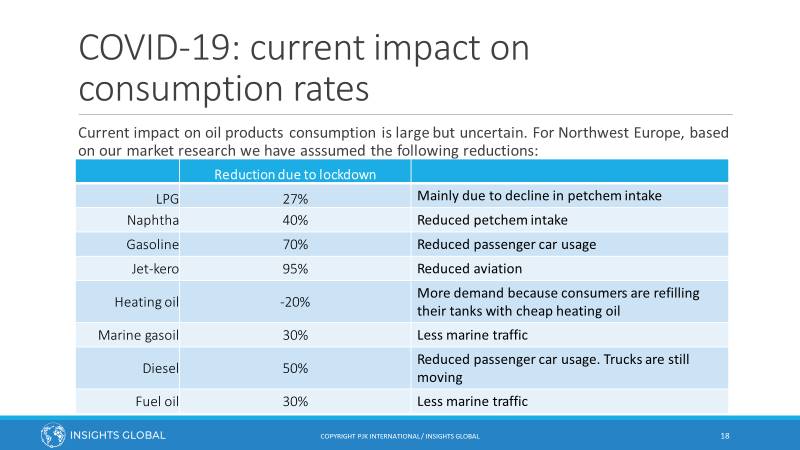

As we all experience the impact of Covid-19 is huge on our daily life and therefore also on our fuel consumption. The Corona effect needs to be incorporated on the forecasting models. Assumption is that the current lockdown lasts three months and has a negative impact for all fuels with the exception of heating oil. Reduction of diesel and LPG volumes are a bit lower because both diesel and LPG consumption is not limited to passengers’ vehicles. Commercial vehicles like buses and trucks don’t use gasoline fuels but usually diesel or LPG. Jet-kerosene is very much hit as almost all passenger traffic has stopped.

Reduction lockdown

LPG: 27%

Naphtha: 40%

Gasoline: 70%

Jet-kero: 95%

Heating oil: -20%

Marine gasoil: 30%

Diesel: 50%

Fuel oil: 30%

Reduction after lockdown in 2020

9%

13%

23%

32%

-3%

10%

17%

10%

After the lockdown, consumption level will gradually normalise, which will take five years. However, it is unclear yet what the exact impact of Covid-19 will be on the travel behaviour of people.

IMO 2020

The International Maritime Organization (IMO) has implemented its global legislation to limit sulphur emissions as a result of marine fuels. The legislation calls for a reduction of the sulphur content in marine fuels to less than 0.5%, which has started January 1st, 2020. Until the start of 2020 the limit was 3.5%. The first months of 2020 show that VLSFO seems to be the dominating bunker fuel. Consumption of MGO increased only slightly by around +10%. HFO is about 15-20% of total fuel oil consumption, with the rest being mostly VLSFO.

The consumption of bunker fuel is heavily correlated with global trade, so we expect it will take several years before bunker fuel market is at the same level as in 2019. However, terminals in ARA specialized in fuel oil will benefit from the growing size of the fuel oil bunker market. As the number of grades has increased and more components are needed to blend into the 0.5%FO / HSFO / MGO, more storage capacity is needed.

Additionally, on top of these structural effects on fuel oil supply, demand and imbalances, there is an enormous oversupply in the market due to the COVID-19 / Corona crisis. This has resulted in a steep contango in fuel oil forward prices and is stimulating traders to buy and store excess fuel oil supply. This provides major support for fuel oil storage rates in the short to medium term.

Electrification of passengers’ cars

Electric mobility is growing very fast. In 2018, the global electric car fleet exceeded 5.1 million, up 2 million from the previous year. China sold over 1 million cars in 2018, followed by Europe (385,000) and US (361,000). Norway has the highest market share for sales (46% in 2018). According to the IEA the projected growth in the New Policies Scenario of electric vehicles would cut oil products by 2.5 million barrels/day.

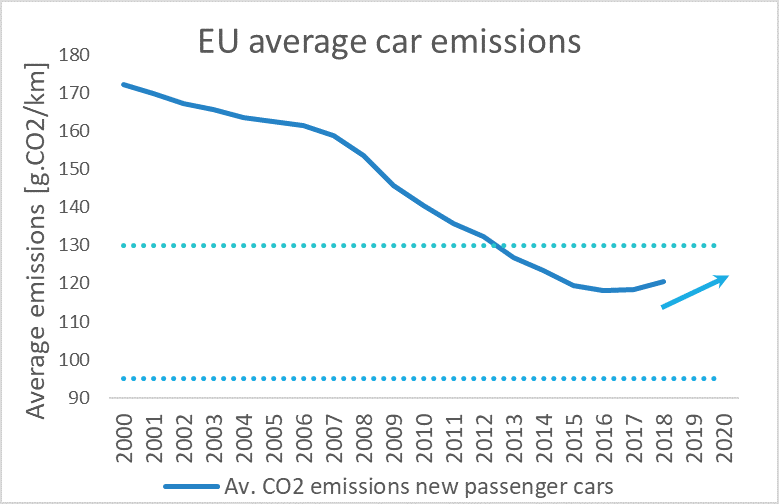

In a push to limit GHG emissions originating from vehicles the European Commission has imposed emission targets to car-producers. New cars are tested and need to have CO2 emissions lower than a certain limit. This limit has been gradually lowered to an average of 130 gram per kilometre in 2015 and will be lowered even further to 95 gram per kilometre as from 2021. CO2 emissions are directly proportional linked to fuel efficiency and therefore have a direct effect on consumption volumes per car per kilometre. As from 2025 the EU emission target is -15% relative to 2021. As from 2030 the target is set on -37.5% relative to 2021.

If car manufacturers do not comply to these targets, they will get penalties because of non-compliance. As BEV’s count as zero emissions cars, it is expected that these targets drive the production of electric cars.

However, reality is different as EU average car emissions are increasing again, see figure 5.6b. Higher SUV sales and not diesel decline have resulted in higher CO2 emissions.

Nevertheless, this electrification trend will have an impact on the gasoline consumption. In ARA the port of Amsterdam plays a central role in the gasoline segment. Because Europe has a structural surplus of gasoline there is a continuous flow being exported out of Europe to gasoline outlets. Consumption of European gasoline is expected to decrease, mainly because the electrification of its car fleet. As the production of gasoline will not decline or not decline that fast, it is expected that the surplus of gasoline will increase, which is beneficial for terminal operators.

Reverse dieselization of European passenger car sales

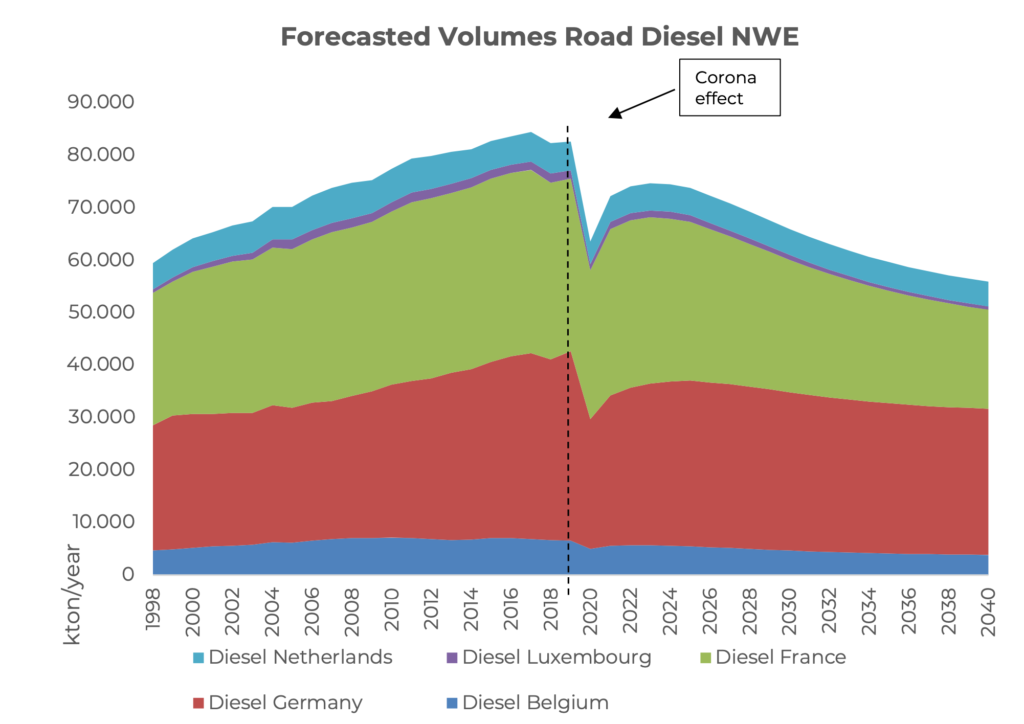

Due to a mix of governmental policies and changes in consumer preferences the share of diesel-powered cars relative to total cars sales has shifted dramatically in Northwest Europe. Consequently, the consumption of diesel is decreasing and it is expected this trend will continue. As production of diesel will not decline or not decline that fast, the deficit of gasoil / diesel is expected to decrease, which is not beneficial for terminal operators.

Conclusion

Although the oil market is really hit by Covid-19, the direct impact on oil terminal operators is positive as the market is currently in a deep contango. Consequently, tanks are rented out and storage fees have increased significantly.

Other themes like IMO 2020 and electrification of passenger cars seem to have positive effects on the profitability of terminal operators. IMO 2020 create more tank storage demand because of a higher number of bunker fuel grades and more components that are needed, while for gasoline the structural imbalance is expected to increase.

However, for the storage demand for diesel is expected to decrease because the current deficit is expected to decrease.

Having access to accurate, up-to-date oil storage rates is crucial to make the right business decisions.

With our Global Oil Storage Rate Report, you’ll gain access to the single and only authoritative source of storage rate information available worldwide. It will provide you with transparency on price levels in global tank storage markets regularly, so you are always in the know and can set the right ask and bid prices for your storage.

Download your FREE Sample Report now and discover what information you could have at your fingertips each quarter.

As we are now in the second quarter of 2020 it is time to look back on the introduction of the IMO legislation on the regulation of sulphur emissions from bunker fuels. The dust has settled with respect to the implementation of these new rules. But as this happened a ‘black swan’ arrived on the global oil scene: COVID-19 or the Corona virus. This virus and the international crisis it evoked is gripping international trade and impacting shipping and bunker sales like nothing we’ve ever seen before. So, this article will also look forward to estimating the medium-term impact on bunker markets and in particular on bunker storage markets.

Running up to 2020

The International Maritime Organization (IMO) has implemented its global legislation to limit sulphur emissions as a result of marine fuels. The legislation calls for a reduction of the sulphur content in marine fuels to less than 0.5%, which has started January 1st, 2020. Until the start of 2020 the limit was 3.5%.

Leading up to the start of this new era in marine fuels there have been multiple opinions or scenarios about which bunker fuels would become dominant. In first instance, most stakeholders thought HSFO would remain the dominant bunker fuel because of the expected uptake of scrubbers. Other stakeholders assumed that MGO would become the dominant bunker fuel as there wouldn’t be enough supply of 0.5% FO. In 2018/2019 some oil majors, IEA and consultants changed their opinion believing that VLSFO would become the dominant fuel. There were other stakeholders, like the gasoil traders, who thought that the demand of MGO would increase significantly because of IMO 2020.

The first months of 2020

The first months of 2020 show that VLSFO seems to be the dominating bunker fuel. Consumption of MGO increased only slightly by around +10%. HFO is about 20% of total fuel oil consumption, with the rest being mostly VLSFO.

The introduction of the new 0.5%FO, called VLSFO, has led to some compatibility concerns. VLSFO blends can come from residual components and distillate components. Residual components are mostly aromatic due to the asphaltenes in the bottom of the barrel. Distillates are high on paraffins. Blending these two streams together can lead to compatibility issues. This can occur if a ship switches between different batches and the fuel is mixed in the ship’s fuel tank, a process also known as co-mingling. Co-mingling bunker fuels from different origins could lead to serious damage to engines or clogging of fuel lines. VLSFO residue blends, being more aromatic and hydrotreated vacuum gasoil (VGO), being less aromatic have these compatibility issues.

These compatibility issues also have a positive impact on the demand for storage capacity as some product owners avoid co-mingling new fuels in their tanks. So, this calls for segregated tanks, which will increase demand for tanks.

An important and lucrative business for oil traders in the ARA-region used to be the transhipment of fuel oil from Russia to the Far East. However, this transit flow has largely disappeared. On the one hand supply of Russian fuel oil has gone down whereas demand for fuel oil in Asia has dropped significantly. Furthermore, Asian bunker demand for fuel oil is currently be supplied from other sources more nearby. Nowadays, Russian export are directly exported in smaller tankers, with as main destination the US. ARA is not the place anymore where making bulk for HFO takes place.

Looking forward

Our assumption in the post 2020 era is that the shipping industry will keep on using FO as the dominant marine fuel (80%). Unclear is what the share of each VLSFO and HSFO will be.

In our forecasting models the Corona effect is incorporated. Assumption is that the current lockdown lasts three months and has a negative impact on marine fuel bunker consumption levels. After the lockdown, consumption level will gradually normalise, which will take five years. Our assumption of five years is based on experience in the past and the enormous fall of GDP which influences the consumption of fuel oil. IMF forecasts a contraction of the global GDP of 3% in 2020, while the Eurozone will see a decline of 7.5% in 2020. It will take several years of GDP growth to be back at the same GDP level as in 2019. The consumption of bunker fuel is heavily correlated with global trade, so we expect it will take several years before bunker fuel market is at the same level as in 2019.

Due to growing bunker fuel consumption and declining average production, surplus in NW Europe will change into a deficit. Terminals in ARA specialized in fuel oil will benefit from the growing size of the fuel oil bunker market. As the number of grades has increased and more components are needed to blend into the 0.5% FO / HSFO / MGO, more storage capacity is needed.

Additionally, on top of these structural effects on fuel oil supply, demand and imbalances, there is an enormous oversupply in the market due to the COVID-19 / Corona crisis. This has resulted in a steep contango in fuel oil forward prices and is stimulating traders to buy and store excess fuel oil supply. This provides major support for fuel oil storage rates in the short to medium term.

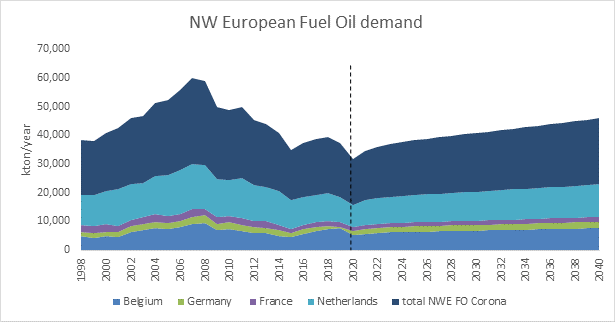

Figure 1: NWE HFO demand Forecast

So summarizing, the introduction of IMO 2020 fuel oil regulations and the COVID-19 / Corona crisis have had the following impact: 1) More tanks needed to segregate blend and fuel grades 2) Less arbitrage flows limit demand for large tanks 3) Long term bunker demand growth and rising imbalances will support tank demand 4) Short to medium term support of fuel oil storage rates due to steep contango

The real impact of Corona on the global and regional GDP’s is not clear yet, but we may conclude that the IMO 2020 regulation have had a positive impact on the ARA tank storage demand. Also in the short to medium term, the COVID-19 / Corona crisis have had a positive effect on the tank terminal business.

The COVID-19 virus has a huge impact on the global oil market. The virus and the economic crisis it evoked results in a large decline of the oil demand. I this article we will describe the consequences of this drop in consumption on the tanks storage demand in main oil hubs.

A collaboration between Q88 and Insights Global, updated version

In the world of the liquid storage some 5,000 terminals can be identified. These terminals have different kind of functions. A terminal’s main function is to balance supply with demand, they can act as import terminal, as trading platform or offer strategic storage options.

Q88 and Insights Global are proud to partner to bring our clients timely information. Never before has the relevance of these terminals been highlighted, and in this article we will analyze the recent confluence of events including 1) super contango due to OPEC+ conflict and 2) demand destruction due to the COVID-19 crisis, impact tanker vessel visits, and berth occupancy at the four major trading hubs.

In the international oil and petrochemical market four main trading and storage hubs can be distinguished: ARA (Amsterdam-Rotterdam-Antwerp), Houston, Singapore and United Arab Emirates (UAE). Due to their large consuming backyard, their refinery infrastructure base and presence of a trading or financial industry, these hubs have become dominant regions in this trading industry.

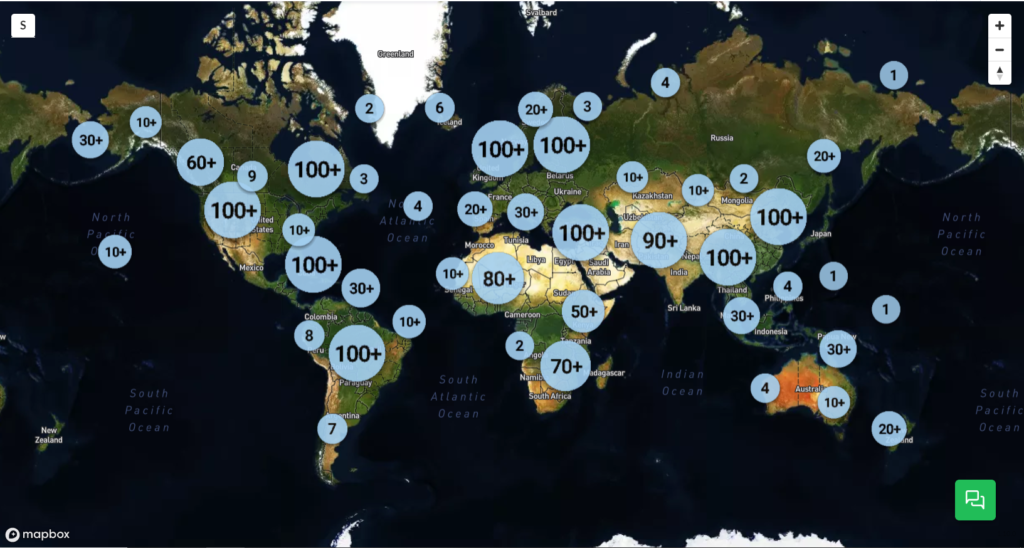

Figure 1: Location of tank terminals around the globe; source TankTerminals.com

More details of the key trading hubs

The ARA consist of 68 terminals with a total capacity of around 36Mcbm. From these terminals, 65 terminals are marine terminals. Based on capacity the most dominant player is Vopak (9.2Mcbm) followed by Koole (3.5Mcbm), VTTI (3.2Mcbm) and Oiltanking (3.2Mcbm).

The port of Houston has 52 terminals with a capacity of approximately 29Mcbm. Main players are Kinder Morgan (6.3Mcbm), Enterprise Products (4.7Mcbm) and Magellan Midstream (4.2Mcbm). Of these terminals, 35 terminals have barge access and 24 terminals have sea access.

Singapore has 21 terminals with a total capacity of 16Mcbm. The biggest storage player in this area is Vopak (3.3Mcbm), followed by Oiltanking (2.5Mcbm) and Universal Group (2.3Mcbm).

The UEA consists of 61 terminals with a capacity of 18.5Mcbm. 20 of these terminals have sea access and 11 have barge access. The most dominant storage player is Vopak (2.6Mcbm), ADNOC (2.3Mcbm) and Horizon Terminals (1.7Mcbm). All these terminals are marine terminals.

“When deep-diving the global tank storage market and specific areas, it absolutely essential to understand how many storage capacity there is, how many players are active and what their position is”, according to Jacob van den Berge, Marketing and Sales Manager at IG. “This is the first step in defining the competitive landscape of the industry.”

Major events and their impact on storage demand further explained

Super contango due to OPEC+ conflict

What is contango? A contango is a situation where the price of front month oil futures is lower than oil with future delivery. If the spread between these prices is large enough to cover storage, finance and shipping costs, a trader is able to make a profit by buying oil now and selling it on the futures market for a later delivery. However, in order to capitalize on this profit, a trader needs storage (and transport) capacity. That is what happened in the first quarter of 2020 with massive demand for storage in ARA and the other key trading hubs resulting in high occupancy rates, putting a premium on free tank capacity now.

As the contango market structure persists and there is a lack of onshore storage facilities, traders are turning to tanker vessels to store their precious hydrocarbons.

This situation was heightened when Russia and Saudi Arabia could not come to terms regarding the height of production cuts to stabilize the fall in oil prices and Russia stepped out of the OPEC+ alliance. This resulted in Saudi Arabia offering its crude with huge discounts to its international customers, which triggered a free fall of oil prices and resulted in a super contango.

The recent peace between these two top producing countries and the subsequent OPEC+ deal has only reduced the speed of oil prices declining. The recent negative WTI oil prices show that we are far from balancing the market.

“Having an understanding of these key issues is imperative while calculating potential earnings,” says Chris Aversano, Product Manager at Q88.com. He continues, “Many of our products have earnings estimators that are built-in, giving our clients a greater understanding of the marketplace.”

Demand destructive impact of COVID-19

As we know, Coronavirus originated from China, and initially affected only China and its enormous economy. However, as the virus spread, different government lockdown interventions were initiated and economies came to a standstill. Less consumption, less production, less trade and less investments caused demand to be reduced significantly, all occurring in the first quarter of 2020.

A new feature in TankTerminals.com, called the Logistical Performance Benchmarking add-on, enables us to see what’s going on at terminals on a weekly basis. Amongst others, we can look at the activity levels at tank terminals.

So what did the numbers at the terminals of these major trading hubs show? Is there any impact of the super contango and COVID-19 crisis visible?

Putting It All Together

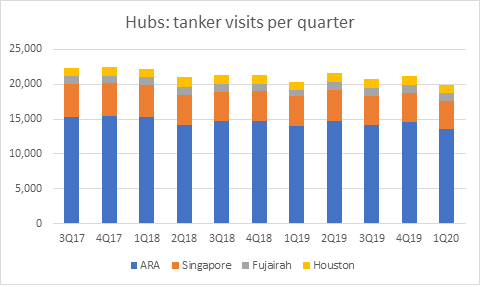

Tanker visits per hub per quarter

In figure 2 it can be seen that the number of tanker vessels visits at the marine terminals of the different hubs, ARA and Singapore show a similar pattern as applies for Fujairah and Houston. For ARA and Singapore applies that the peak of the visits were at the end of 2017 and the least visits in the first quarter of 2020. For Houston and Fujairah applies that highest number of tanker visits was in the second quarter of 2018 while the lowest number of tanker visits were seen in the first quarter of 2019.

Figure 2: Tanker visits per hub per quarter; source TankTerminals.com

The maximum value in ARA was 15405 tanker visits and the minimum value with 13591. In Singapore, the maximum value was 4756 and the minimum value was 3956. For Fujairah the maximum value was 1196 and the minimum value was 878. The maximum value in Houston was 1372 and the minimum value was 1153. As can be derived from the number of tanker visits, the ARA region accounts of almost 68% of all tanker visits of these four hubs combined. This is because of the extensive use of tanker barges and coasters in this area to distribute products within Europe.

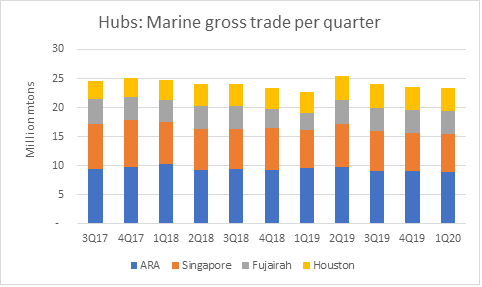

Marine gross trade per hub per quarter

Marine gross trade is calculated with the DWT of tanker vessels that loaded and discharged at a certain terminal. When we look closely at the marine gross trade trend and we compare that to the number of tanker visits, we are able to distinguish a similar trend as seen in figure 3 below.

Figure 3: Marine gross trade per hub per quarter; source TankTerminals.com

It is evident that the marine gross trade of the different hubs are more in line with each other. ARA accounts for 38%, Singapore 32%, Fujairah 18% and Houston 12% of the total sum of marine gross trade within these four regions. ARA is known for its intra- and inter- regional barge transports which contains lots of tanker visits with low volumes of product. Houston has a lot of push boat transports which are not included in this tool’s coding. Furthermore, we excluded Galveston and Beaumont area from the numbers.

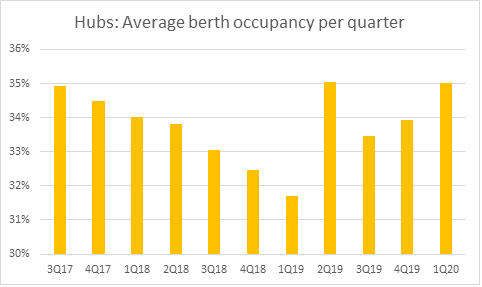

Berth occupancy per hub per quarter

Berth occupancy rates per region show a diverse picture on a quarterly base. However, some sensible deduction can be derived from looking at the data. For the regions ARA, Singapore and Houston, the average berth occupancy rates per terminal show a rather stable picture per quarter with minimum values around 31-32% and maximum values around 34-35%. Fujairah has a relatively inconstant structure with a minimum value at around 29% and maximum value just below 40%.

Figure 4: Average berth occupancy per quarter; source TankTerminals.com

It is evident from the chart above that the average berth occupancy rate for all hubs combined is the second highest in the first quarter of 2020. Across all regions, the data implies that average berth occupancy in this quarter is far above the average value. The decreasing trend up to the first quarter of 2019 highlights the ‘wait-and-see’ attitude leading up to the IMO 2020 marine fuel implementation. The peak in berth occupancy rates in the second quarter of 2019 and subsequent increases in berth occupancy since then can be explained as terminal operators were preparing for IMO’s legislation that went into effect at the beginning of 2020.

Conclusion and what is next?

When looking at the statistics of tanker visit numbers, marine gross trade and average berth occupancy rates, it can be concluded that the main trading hubs show similar patterns, especially in the second quarter of 2020 in which the defining events OPEC+ conflict and COVID-19 evolved.

In the first quarter of 2020 the number of tanker visits of the different hubs was at a minimum while the average berth occupancy rates were at their second highest. The low number of tanker visits is likely to have been caused by 1) high fill rate, or almost full tanks of terminal operators due to contango storage play options and 2) lower consumption levels due to demand destruction by COVID-19.

The high berth occupancy rates can be explained that, despite the low number of tanker visits, in the first quarter of 2020 terminal operators were coping with the impact of COVID-19 to their business operations which might have resulted in a bit slower vessel handling at the terminals.

“Knowing how well your ships are performing is crucial during these uncertain times,” say Chris Aversano, Product Manager at Q88. He continues, “Our VMS system gives the owners peace-of-mind to make the right decision at the right time. Additionally, our Position List platform allows for brokers to better serve their clients in a highly competitive and continuously changing space.”

Jacob van den Berge, Marketing and Sales Manager at IG adds: “using different data sets, combining this with our own unique knowledge and expert knowledge of our partners such as Q88 has proven to offer unique market intelligence. This supports our relations in making justified commercial decisions.”

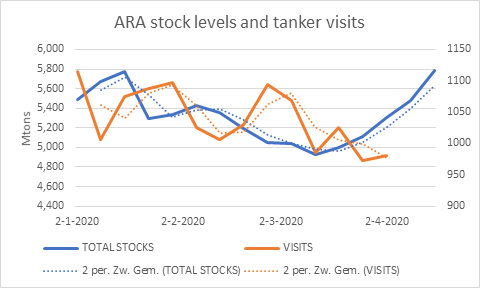

According to figure 5 below, when we focus in at the first quarter of 2020 and look at the tanker vessel visits in ARA on a weekly basis we see the number of tankers at terminal’s berths are all below this time series weekly average. If we than look at the ARA oil product stocks levels for the same time-period, we can actually see a buildup of stock levels since March 12. This in line when the lockdown measures that were initiated by the European governments.

Figure 5: ARA stock levels and tanker visits; source TankTerminals.com

Having access to accurate, up-to-date oil storage rates is crucial to make the right business decisions.

With our Global Oil Storage Rate Report, you’ll gain access to the single and only authoritative source of storage rate information available worldwide. It will provide you with transparency on price levels in global tank storage markets regularly, so you are always in the know and can set the right ask and bid prices for your storage.

Download your FREE Sample Report now and discover what information you could have at your fingertips each quarter.

The world is in crisis mode. The Corona virus is gripping humanity, leading to lockdowns, overcrowded hospitals and thousands of casualties. Oil markets are also heavily impacted. As a direct of effect of the Corona lock downs global oil demand plummeted. The OPEC+ cooperation also exploded. Russia and Saudi Arabia couldn’t agree on output cuts. As a result an outright fight for market shares erupted between both heavyweights with oil prices collapsing as a consequence.

Oil markets are totally out of balance. The demand destruction due to the many lockdowns around the world combined with the production increases coming from Arab Gulf States is leaving global markets oversupplied. Estimates range from 10mb/d to 20mb/d. Quite a big range, so no-one really knows how much. But one thing is certain: it’s a very big number. And there is no end in sight. Petroleum markets are notoriously slow in balancing out. Supply is slow to react to low oil prices as costs of maintaining production levels are low. The unit costs associated with crude oil production are mostly costs associated with exploration, drilling and completing wells. After this is finished these are sunk costs, so not relevant anymore. As a result producers will keep pumping oil until prices hit rock bottom.

Due to the oversupply situation a contango emerged on futures markets. In a contango situation prompt oil prices are lower than forward oil prices. Traders are stimulated to buy crude or oil products on the spot market, in order to increase demand, and put this oversupply into storage so that they can sell it on the futures market for higher prices and for delivery somewhere in the future. The contango is there to enable traders to earn money on this play. Otherwise they would not be encouraged to buy crude and oil product from producers because there is no demand. This is called storage arbitrage and this is perfectly in line with what the markets need: filling up tanks to store the oversupply and decreasing oil prices to limit production rates and stimulate consumption.

Who is profiting?

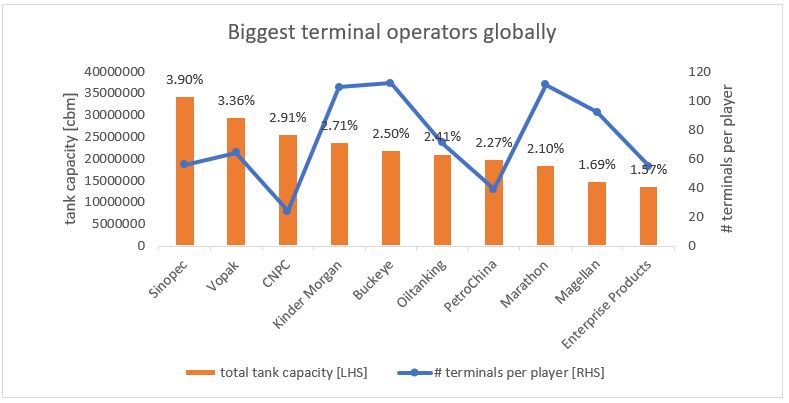

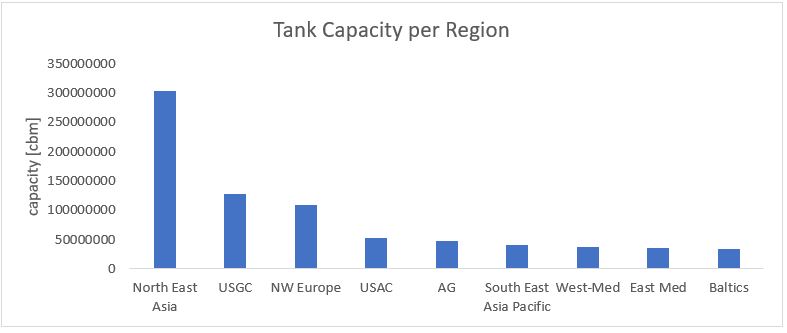

The contango has prompted a run on tanks. If you are able to find free tank capacity now you can make a fortune. Tank terminal owners are, despite the current depressed economic situation, in the best position that they can imagine. But who are these ‘winners’? See below a graph showing the global top tank owners.

Also globally tank capacity is distributed unevenly and mostly concentrated in hubs. See below for tank capacity per region. As you can see North East Asia, with China included, the country where the outbreak started, has the most tank capacity. The USA and Europe are second and third in this ranking order.

For oil markets it is of vital importance to have spare tank capacity to absorb imbalances. However, the current oversupply is immense. How long will it take until global tank storage capacity is full?

Let’s assume that current oversupply is on average around 10mb/d for the coming months. It is probably higher right now but may decrease after the situation becomes normal again and the various lock downs and measures to contain the virus are lifted. Looking at current stock levels in the main hubs, ARA, USGC, Fujairah and Singapore, we see that approximately 75% of commercial tank capacity is full.

That leaves only 25% to go until tank capacity has reached tops. If we assume that this 25% applies to all independent tank capacity globally we can calculate, using global crude and petroleum products tank capacity and correcting for strategic petroleum reserves that are assumed to have a much higher utilization rate, that it will take about 112 days or almost four months for tanks to reach their full capacity.

After tank terminals are full the next most economic option is to charter vessels and use these vessels as floating storage. According to various sources we are already seeing this happen in shipping markets. So in reality, because the combined storage capacity is simultaneously being filled up, it might take a little bit longer for tanks to fill up.

In any case our ARA oil products stock data, Rhine flow data will give a good view on developments in European storage. If you require data to understand global tank terminal capacity our TankTerminals.com database is a vital piece of information you can use, either for analysis or to find free tank capacity. Let us know if you need anything!

Oil storage tanks will fill up quickly. Due to the corona crisis, planes and cars remain unused. Meanwhile, due to a conflict between Russia and Saudi Arabia, additional oil is poured into the market. Storage tanks are expected to be full within a few months. What happens then?

It is unprecedented how much demand for oil has decreased because of the corona virus. As a result, oil prices came under pressure early this year. OPEC countries wanted to limit oil production as well as countries that are not members of OPEC. Russia refused, after which Saudi Arabia decided to increase production to lower the price.

Futures trading

There is an overproduction of oil and there is only one way out: store hydrocarbons. The storage tanks are filled even faster due to the price structure that is now developing on futures market, explains Patrick Kulsen of market research and consultancy company Insights Global. On their tankterminals.com platform, the company has a global database listing all indepedent storage terminals. “In the oil market you have futures trading. This means that you can now buy oil for a delivery in, say, a year. In the meantime, you have to store the oil. This market has accelerated because traders can now buy the oil for a low price and sell it at a high price on the futures exchange. The market is in contango, so the tanks fill up in no time. “

A few months

Kulsen thinks storage tanks will be “or faster” full within six months. Research agency Rystad Energy also thinks that onshore tanks will all be filled within a few months. If that happens, it is still possible to divert to oil tankers, but that storage is more expensive. According to Rystad Energy, that capacity is probably not enough either. Many Very Large Crude Carriers (VLCC) are already in use. Also, the cost of renting a VLCC within a month has gone from about $20,000 to between $200,000 and $300,000.

Local generation of wind, solar, hydro and

nuclear power, renewable heat and energy conservation together will greatly

reduce our dependence on oil, gas and coal exporting countries. Will the energy

transition put an end to energy trade?

For most countries, energy independence is just a dream

For nations that never had the luxury of natural resources, renewable energy provides a great opportunity to lessen the dependance on international energy trade. The same goes for nations that already depleted all economically viable reservoirs.

Consequentially, national energy self sufficiency often has been mentioned in support of the energy transition. Self sufficiency however should not be a goal in itself. Costs minimization has been the reason that energy trade has surged over the last decades. Imported coal, oil and gas often simply provide cheaper energy than can be sourced locally.

Costs will of course still be relevant in a carbon constrained world. Regions with favorable climate, favorable geography, low population density, a fleet of operational nuclear power plants or a pragmatic stance on carbon capture will be able to produce low carbon energy far cheaper than less advantageous parts of the world.

It would be naive to suggest that clean energy will not be traded

If the whole world strives to reduce carbon emissions, front runner countries will reach carbon neutral self sufficiency faster than others. From that point on, some countries will almost certainly be able to reduce emissions faster and cheaper via trade than by continuing to strive for total self sufficiency. If part of a country’s energy demand can be met cheaper via imported low carbon energy, low carbon energy will be traded. There is no sound reason not to.

The challenge now is to predict in what forms renewable or low carbon energy will be traded. What will be the commodities of the future? Six likely contenders:

Electricity

Electricity is the fastest growing form of low carbon energy. As a commodity, low carbon electricity is indistinguishable from electricity generated in conventional power plants. Low carbon electricity is fully compatible with existing infrastructure for power transport and distribution. New high capacity power lines enable power trade not just between neighbouring countries but also across whole continents. The problem with electricity is that long term storage is complicated and expensive due to the relatively low energy density of batteries.

Hydrogen

Hydrogen is an energy carrier that can be produced practically carbon neutral. From fossil fuels with carbon capture or via electrolysis using low carbon electricity. As a gas, hydrogen can be transported in bulk via pipelines. Some existing natural gas infrastructure might be repurposed for hydrogen. Below -253 degrees centigrade, hydrogen becomes an energy dense liquid that can be shipped or stored in cryo tanks

Methane, methanol and other hydrocarbons

Methane is a fossil commodity but can also be produced from biomass. Using hydrogen and (non fossil) carbon dioxide, methane can also be synthesized carbon neutral. The same goes for methanol, various oils, lactic acid and almost all useful hydrocarbons that currently are produced at scale from fossil oil. Low carbon variants are chemically identical to current commodities and can make use of existing infrastructure.

Ammonia

Ammonia is a commodity currently produced and traded in bulk for the production of fertilizers and other chemicals. Ammonia nowadays is made mostly from fossil methane but it can be produced carbon neutral using hydrogen and nitrogen. Low carbon ammonia can replace current industrial ammonia consumption. Ammonia itself can also be used as a fuel or as an easily liquefied carrier for transport of hydrogen.

Metal powders

Metal oxidation is a natural process that can be sped up by increasing temperature and exposed metal surface. Metal powder in a flame burns at high temperature. Oxidized metal powder can be regenerated using low carbon electricity or hydrogen. Iron, alumina and other metals are already global commodities. Creating metal powder might be done before transport or on site where stored energy is consumed.

Biomass

Biomass is a low carbon commodity that already has some traction as renewable commodity. Wood chips, pellets, bio-ethanol, biodiesel are the only carbon neutral energy carriers that are already traded at scale between continents. Further scaling however is bound by natural growth rates. Biomass is only carbon neutral if the regrowth of trees and energy crops is in balance with bioenergy consumption.

No clear winner, potential for all

In non carbon neutral form, all potential global energy commodities mentioned above already have their applications in our current carbon intensive economy. Most of those industries will stay just as relevant in a carbon constrained world. For all mentioned carbon neutral commodities therefore it is reasonable to at least meet current consumption without carbon emissions.

Carbon neutral electricity has a head start in replacing its fossil counterpart. Electrification of mobility, heating and some industrial processes furthermore assures that the relevance of electricity will grow in a carbon constrained economy. Except for biomass, all other proposed commodities will also be produced mainly using low carbon electricity.

Which future commodity eventually will replace fossil oil as the world’s main energy carrier, will be decided by energy losses in conversion, practicalities in handling, storage and transport, geopolitics and of course first mover advantages. The transition has started, it’s time to place your bets.

Geographical price differences will lead to increased trade! In this article we would like to highlight the subject arbitrage and what this theme has for impact on the tank storage market.

Introduction arbitrage economics

In theory (Investopedia), arbitrage is the simultaneous purchase and sale of an asset to profit from a difference in the price. It is a trade that profits by exploiting the price differences of identical or similar positions on different markets or in different forms. Arbitrage exists as a result of market inefficiencies.

But how does this work in practice? As commodity trading firm Trafigura describes on their website, they apply three forms of physical arbitrage:

1 – Geographical arbitrage identifies temporary price anomalies between different locations;

2 – Time arbitrage seeks to benefit from the shape of the forward curve for physical delivery (see our article on market structure); and

3 – Technical arbitrage seeks to benefit from the different pricing perceptions for particular commodity grades and specifications

In this article and to make things clear we will focus solely on geographical arbitrage and in particular the Northwest European Singapore arb for heavy fuel oil.

In order to calculate heavy fuel oil’s price difference between Northwest Europe or ARA and Singapore, we compare the FOB ARA spot price with FOB Singapore swap price, second month due to the duration of the voyage. The difference between these values is the spread and should be large enough to cover the trade costs.

On most occasions heavy fuel oil is shipped to Singapore in a VLCC (Very Large Crude Carrier/310 kt DWT) and loads approximately 270 kt of product. We therefore sum the VLCC freight rate, finance costs, port costs, inspection costs and demurrage to come to total trade costs. Should the spread be more than the trade costs the arb between both regions is open. When the spread is less than the trade costs the arbs is closed. T

Importance of arbitrage for tank storage companies

So monitoring if arbs are open (or closed) is a good indication, to understand if trade between two regions is likely to increase. A positive trading environment, ultimately will influence tank storage dynamics.

Please note that arbitrage cannot be seen as a single indicator for business opportunities for tank storage companies. Other indicators that should be taken into account are: price volatility, market structure, and more. These subjects have been highlighted in other articles.

The market structure stimulates traders to buy now and sell late. In this article we would like to highlight the themes contango and backwardation and what market structure means for tank storage operators.

Market structure – Introduction to contango and backwardation

An oil price for immediate delivery is called spot price or cash price while an oil price for delivery at a specified date in the future is called a forward price. When we plot these various prices and order them from short to long term delivery, a forward curve is created.

When a futures price (second month) is below a futures spot price (first or front month), the market structure is in backwardation. In this case, the forward curve is downward sloping. When the futures spot price is below the futures price, the market structure is known as contango. In this case, the forward curve is upward sloping.

A contango usually occurs when supply is higher relative to demand (supply glut) while in a backwardation demand is higher relative to supply (shortage). As time evolves, an oil forward curve can switch from backwardation into contango as in the case of the NYMEX RBOB futures forward curve. When a cyclical pattern is visible, this is called seasonality.

With respect to NYMEX RBOB futures, US gasoline prices tend to rise towards summer driving season during the period June and September. In the period before peak demand, oil traders tend to buy and store products to have product available in times of high consumption.

Importance of market structure for tank storage companies

In a period of contango, oil traders are encouraged to buy oil products today and sell in the future when the spread between two months covers storage, shipping and finance costs. When this opportunity presents itself, product is being sold, shipped and stored, resulting in more business for tank storage companies. This play is known as a ‘contango storage play’ but is limited by the maximum tank storage capacity available.

In some rare occasions, when the time spread is large enough even tanker vessels are chartered by trading companies to store oil products. This is known as floating storage. In this rare environment demand for tank storage is high and pushes storage rates for spot availability. Backwardation discourages storing oil products as a trader can sell oil today at a better price than in the future.

Is market structure the only business opportunity indicator for tank storage companies?

There are other indicators that should be taken into account such as price volatility, arbitrage and more. These topics and Insights Global’s market model will be covered in upcoming weeks.