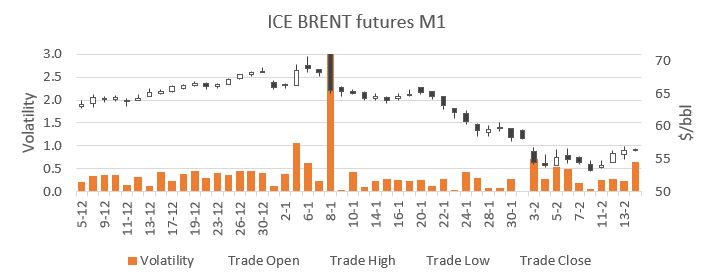

Volatility is applied to describe fluctuations of oil prices and it relates to the level of uncertainty in the market. Historic volatility is calculated by the standard deviation of an oil price return series, measured during a certain time frame

Introduction to Price Volatility

Price volatility will stimulate traders to buy low and sell high. In this article you will learn about it and how it influences demand for tank storage.

There are other ways to calculate volatility i.e. looking at the daily high and low range of oil prices during a trading session or the estimated volatility of an option (implied volatility). Implied volatility offers an outlook on the expected volatility and is the opposite to historic volatility that looks back into recent history. It is important to understand that there are events that can impact the level of price volatility.

When analyzing the Brent crude price and periods of high volatility there are a number of time frames when crude futures prices dropped while volatility expanded. Like on January 8 (weaker geopolitical risk premium), and February 3 (worries of Corona to demand for oil).

Importance of price volatility to tank storage companies

Important for tank storage companies to understand is that in times of high volatility, such as described in these three cases, trading volumes on the paper market are very high. As traders are able to make bigger profits in a high volatile regime when an old saying become reality: ‘buy low and sell high’.

Taking into account that every paper position is squared by a physical position, one can understand that also physical trade will increase. More physical trade will eventually lead to more demand for tank storage capacity.

Is price volatility the only business opportunity indicator for tank storage companies?

There are other indicators that should be taken into account such as market structure, arbitrage and more. These topics and Insights Global’s market model will be covered in upcoming weeks.

The use of crude oil, natural gas and coal has been a primary driver of human progress. Unfortunately, now we know that the use of fossil resources is also a primary driver of anthropogenic climate change. What can be done in the short term?

Every tonne of carbon emitted counts

In 2050 and thereafter, cheap and abundant energy will still be of utmost importance for human progress. The big difference is that this energy will also have to be carbon neutral.

Until all of our energy is sourced carbon neutral, every ton of carbon (not) emitted counts. In the coming decades, it will be fairly easy to do without our most carbon intensive energy source: coal. Substituting oil and gas will however be far more difficult. In the short run, the use of gas may very well increase because of climate policy. Gas fired power plants pollute substantially less than coal fired power plants. Trends in oil consumption for the coming decades will be defined by slow but steady reductions in the ‘old’ economies, balanced at first by growing demand in emerging and evolving economies.

Given that oil and gas production, refining and transport will be facts of life for the coming decades, reducing the carbon intensity of oil and gas consumed will be just as important as substituting oil and gas with carbon free alternatives. Here are seven routes that substantially reduce the climate impact of the oil and gas industry.

Electrification of offshore platforms

Using 11 floating windturbines, Equinor will electrify 5 of it’s production platforms. Reducing gasturbine utilization by 35%, the project will cut carbon emissions by ±200,000 tonnes annually. Besides wind power, providing onshore power to offshore projects may also help cut emissions.

Old fashioned plumbing

Leaks in production and transport result in loss of revenue but are nevertheless common. New satellite and drone imagery simplifies the recognition of leaks. Solving leaks, especially methane leaks, reduces the climate impact while increasing the yield of energy companies.

Carbon capture in production

Raw natural gas and oil may contain large amounts of CO2 which have to be removed in order to comply to standards. This is often done directly at the point of extraction. Storing the separated CO2 underground, instead of just venting it into the air, is an effective climate policy.

Utilization of concentrated solar hear

Most of the easily recoverable oil has already been extracted. The remaining, more viscous crudes have to be heat treated before extraction is possible. Normally, steam for this process is produced by burning gas or oil. GlassPoint Solar enables solar heat to replace this fossil fuel consumption.

CCS at refineries

Oil refineries consume large amounts of hydrogen for removing sulphur and other contaminants from crude oil and to convert crude into refined fuels. This hydrogen is produced from natural gas, with CO2 as byproduct. Capture and storage of this pure stream of CO2 is rather easy.

Reduction of gas flaring

Flaring of gas at oil wells in itself is a climate measure, as CO2 from burned methane has a far lower climate impact than the methane itself. Still, routinely burning away gas on site that could just as well be used productively elsewhere should be prohibited as much as possible.

Abandoning unconventional reservoirs

Extraction and refining of oil from tar sands, in the arctic or from shale reservoirs by nature is more carbon intensive than production from more conventional fields. Given most of fossil resources should be kept underground anyway, it’s best to abandon unconventional fields first.

License to operate

At sufficient scale, most of the options mentioned above are not extremely expensive. Given that almost all oil majors have come to terms with the fact that fossil carbon is the prime source of anthropogenic climate change, implementation of measures that greatly reduce the climate impact of operations should be a no brainer.

Furthermore, if oil and gas producers are not yet intrinsically motivated, exposure to cap and trade programs, carbon taxes, shareholder pressure and eventually consumer boycots should help enforce the utilization of renewable energy in production and refineries, the capture and storage of carbon and the minimization of leaks and flaring.

If you are active in oil and gas, now is the time to take action.

Auteur: Thijs ten Brink, Photo: Zbynek Burival via Unsplash Public Domain

Uit cijfers van EY (2015) bleek dat in Nederland ongeveer 16.000 mensen werkzaam waren in de olie en gasindustrie. In hetzelfde jaar in Amerika waren dat zelfs bijna 1.5 miljoen mensen! Hierbij zijn nog niet eens de dienstverlenende bedrijven meegeteld. Het is dus een immense sector!

Het is niet alleen groot qua omvang maar ook qua complexiteit. Veel bedrijven die we tegenkomen begrijpen slechts het onderdeel van de logistieke keten waarin zij actief zijn. Zij missen kennis van de gehele logistieke keten. Juist die andere ketenonderdelen hebben vaak directe impact op de winstgevendheid van hun business.

Een aantal van deze organisaties hebben bij ons de tweedaagse Oil Academy gevolgd. Na de training zijn zij zich beter bewust van hoe de gehele olie -en gas waardeketen functioneert. Zij begrijpen beter hoe de verschillende marktspelers en fundamentals werken. Al bijna 200 deelnemers gingen u voor en waardeerden deze training met meer dan een 8!

Voor meer informatie, vraag onze Oil Academy brochure aan door het onderstaande formulier in te vullen.

To say that the global tank terminal business is large is an understatement. There are more than 4900 tank terminals comprising more than 1 billion cubic meters of storage capacity. The business has grown at a compounded annual growth rate of 3% since 2005 and in coming years another 10% will be added to global tank capacity. Some might argue that capacity has grown too fast and that we are approaching a situation where markets are ‘over-tanked’. But is this really the case? This is a very relevant question for many players. For instance, if you are a business development manager at a terminal operator you need to understand this because it can guide you in determining if and where to invest. Another example are investors. If you are an investor in infrastructure assets you need to understand this in order to decide on investing or divesting in and valuating terminal assets.

Every terminal essentially has a logistics or hub function. This is the prime function. Some terminals are also used as a trading platform by its clients. Physical commodity traders require terminals for their business model. The last function a terminal can have is to store crude or oil products as part of a country’s strategic petroleum reserves. This last function is interesting for a specific terminal operator but from an economic analysis point of view less relevant because it is dependent on specific policies defined by governments. We therefore leave this function outside of the scope of this article.

So we will focus of the logistics and trading platform functions. After careful analysis of these functions and the value it can bring to clients of terminals we concluded that there are three key factors that act as business indicators for tank terminal markets:

Commodity price dynamics

Inventory levels

Trade flows

If you are analyzing business at a specific terminal you need to look at these factors in the local context. However, for the purpose of this article we have looked at these factors on a global scale and we have focused on oil markets.

Oil price dynamics

Current oil price levels are low and rather volatile. The low price levels stimulates demand and the increased volatility creates trading opportunities. The forward curve is downward sloping (backwardation) which weighs on arbitrage opportunities. However, some institutions like the EIA are forecasting a slight oversupplied global crude market, which could soften the backwardation or even flip it to a contango, which would be good news for the terminal sector.

Inventory levels

Global crude and oil product inventories are on the lower end. This is related to the backwardation price structure. So tanks are slightly underutilized right now.

Trade flows

Global crude and oil products

trade flows have been increasing at a steady rate in the last decade. This rate

resembles the growth rate in tank capacity and thus signals that the balance

between tank capacity and tank demand is more or less balanced. This is a very

positive sign.

The main conclusion from the above analysis is that the global market does not seem to be over-tanked and that the current situation is set to improve significantly after oil price dynamics change to fully support the terminal business. So the future is definitely bright for the terminal business!

About the author

Patrick Kulsen is Managing Director and Senior Consultant at INSIGHTS GLOBAL, a market research company specialized in oil and petrochemical markets. The company’s consultancy team has successfully helped clients with research and commercial due diligence projects for many years. For more information on our consultancy services please follow this link.

In the last decade the tank terminal markets has seen quite a large number of Merger & Acquisition deals. One of the main trends that has been witnessed is that investments funds are stepping in and in many cases are emerging as winners of these bids. As an investor or fund manager you might wonder “Is the tank terminal sector worthwhile getting into?” or “Is the opportunity at hand going to diversify my investment portfolio?”. This blog post will try to give guidance on this subject.

Infrastructure Asset Class

Tank storage assets, due to their resilient and stable revenue profile are considered infrastructure assets. Such assets are attractive investments if it fits the risk/return profile of your fund. Nevertheless there are some nuances that need to be made. Not all terminals are alike so a more detailed approach is needed to distinguish between various groups of terminals. From an investment portfolio perspective it is sensible to group terminal assets into different categories based upon their exposure to business risks.

1. Location, location, location…

One obvious

characteristic is the location of the terminal. For one, country risk is

associated with the location of the terminal. Is the terminal located in an

OECD country or not might be a good way to look at this. However location of

terminals has many more implications. It is the single largest factor driving

value of terminal assets due to various reasons. Most likely if you ask experts

the question “what is are the three most important terminal characteristics”

they’ll answer “location, location and location”. So the conclusion is that a

thorough analysis of the implications of terminal location is needed.

A rather simplistic but effective first order categorization is to group terminals into Hub Location and Non-Hub Location terminals. The hub location terminals are well positioned and are better able the weather downturns in business cycles. Additionally, these terminals are less sensitive to local and regional economic circumstances. Business activity at hub terminals is related to global trade, which is less volatile and thus has a lower risk profile.

Another categorization method is to distinguish between sea-access and inland terminals. This grouping has some overlap with the functional categorization that will be discussed in the next section. Nevertheless it gives additional insights into the risk profile because sea-access terminals offers more flexibility for its customers and has a larger operating region. On the other hand, inland terminals are more restrictive and are in most cases confined to the local area. This doesn’t mean that these assets are worthless, they can be very profitable. However, they do have a different risk profile.

2. Market Segment

After location the second question you need to ask is: what liquid products are stored at the terminal? Products can be categorized into the following main groups: crude oil, petroleum products, pressurized gasses (such as LPG), LNG, chemicals, vegetable oils, bio-fuels and others. For petroleum products and chemicals sub-categories apply, but let’s not overcomplicate matters here. The point is that for instance petroleum product markets have a different dynamic than chemical markets. This translates to a different risk profile for the terminal business. So market segments are a key characteristic.

3. Terminal Functions

A tank terminal can

have one or more functions for its clients. These functions are driven by

business environment and the infrastructure of the specific terminal. The main

functions applicable to terminals are:

-Logistics / hub function:

o Make /break bulk hub

o Distribution & inter-modality hub

o Integration with industrial site

o Bufferstock

-Trading platform:

o Physical arbitrage

o Blending

o Contango storage

o Optionality

-Strategic storage

Uncovering dominant

functions related to the specific terminal that is up for sale gives insights

into its business and the related risks.

Putting it together: does it fit?

By combining the above

mentioned locational, market segment and functional aspects the terminal asset

can quickly be profiled to see if it contributes to the diversification of your

portfolio. A diversified terminal asset portfolio should preferably have a

variety of assets that ranges across different locations, markets segments and

incorporates a varied set of functions. If too many assets are in the portfolio

that have similar risk profiles the portfolio might be too exposed to a certain

risk.

The above mentioned

characteristics have the ability to frame the asset. But please keep in mind

that a more detailed approach is required later on in the process as part of

the commercial due diligence project.

Terminal Portfolio Compatibility Call (FREE)

The above described methodology gives an outline of an approach that can be applied to check if a terminal asset fits your investment portfolio. However, elaborating on all relevant details is outside the scope of this article. Additionally a lot of data is needed to profile terminals. So you might need help to fully implement this method. We can help you with this. Please contact me for a freeandconfidential terminal portfolio compatibility call. In this call, I will apply this method to your investment opportunity so you have instant insights into the risk profile.

About the author

Patrick Kulsen is Managing Director and Senior Consultant at INSIGHTS GLOBAL, a market research company specialized in amongst others commercial due diligence of tank terminals. The company’s consultancy team has successfully helped clients during M&A projects for many years. For more information on our consultancy services, please follow this link.

The tank storage industry is a very competitive market and it brings many challenges to its players. Tank terminal operators for liquid bulk are facing both internal and external factors that can affect the efficiency and the progress of their business.

A few internal factors involve the company’s organization, processes, availability and infrastructure, etc. Terminal operators can be also challenged by external factors, such as competition, regulations and the economy. With more than 7,040 tank storage facilities worldwide, it can be very tough for storage operators to position themselves in the market.

What exactly do terminal operators need to know in order to face their competition?

1 Location

Location for terminal operators is key for the success of their business. Before starting with any terminal construction project, a lot of thought is put into the geographical location of the terminal. In order to analyze the location, a storage operating company needs to have insights on all other players that are active in that area. Besides other factors, analyzing the competition in a certain area can indicate if it is viable to invest in a project.

If a terminal operator already has an existing terminal in a certain region, it is important to know the neighboring competition. Who are those terminal operators? What is their market share? What cargo types do they support? What is the infrastructure of those terminals? All these are a few crucial questions, that terminal operators should ask themselves.

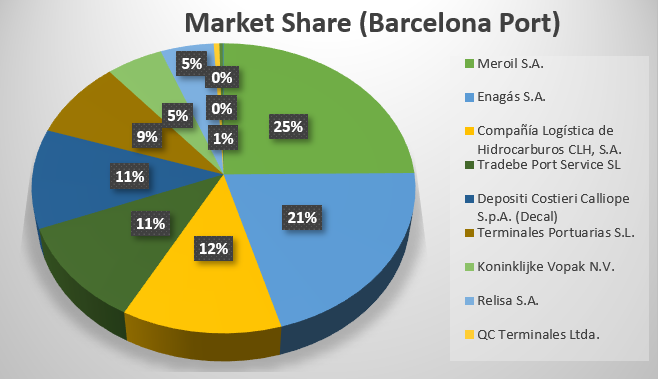

2 Market share and total storage capacity

Another important factor for a terminal operator is to know the largest storage players in the region. This gives the ability for a terminal operator to analyze his/her position in the market and at the same time understand the power of their competition.

How can they easily determine the market share of their competitors? For example, if a terminal operator is interested in Barcelona Port or has an existing terminal in the port, they can look at the total storage capacity of all the terminal operators. In the image below it can be seen how insightful market share is when identifying the biggest players in the port (the market share is drawn from the total capacity of each terminal in the port).

3 Cargo types

For terminal operators it is important to know what cargo types their competitors are able to store. This gives an opportunity for them to create diversity and flexibility in product storage at their terminal. In today’s storage industry, the clients of storage operators see diversity and flexibility as an added value. Thus, there are a few important factors that a terminal operator needs to analyze:

Demand in that region

Production in that region

Import and export flows

Imbalances

Storage availability in that region

4 Different terminal functions and access modes

A tank terminal can have the following functions:

Strategic storage

Logistical storage

Import/Export

Trading hub

These four different terminal functions create different level of competition for terminal operators. Tank terminals that are located in the same trading hub and that are providing the same storage services are in direct competition. A strategic storage that is located next to a logistical storage might not be in direct competition, but terminal operators should still thoroughly analyze the level of competition.

The function of a terminal can also dictate the access modes for a terminal. Terminals can have the following access modes: sea, rail, road, pipeline and barge. A terminal with more access modes can be connected with different international trading markets and provides more options and flexibility for its potential clients.

5 Planned investments and expansions

Terminal operators need to know if there are any new projects or planned expansions in their region. A new terminal can mean stronger competition while a new expansion creates more power to an existing competitor. If terminal operators are aware of the new changes and are properly informed, they can better understand how to face the new challenges.

As the competition is significantly increasing, especially in port areas, terminal operators need to constantly evaluate their infrastructure system and consider expansion possibilities.

What should a terminal operator know about a new project/expansion:

Which company is it and what is their market share?

What will be the total added capacity for an expansion or what will be the total capacity of the new terminal?

When will the project be completed?

What products will the terminal be able to store?

What access modes will the terminal have?

6 Logistical performance

A very important factor for marine terminal operators is to analyze the logistical performance of their competition. This includes the following operations:

Throughput

Berth occupancy

Average visit duration

Tank turns

What does the logistical performance measure?

It determines the productivity and performance of a certain terminal. For a terminal operator, it is a good indicator if the competition is underperforming.

Conclusion:

The six factors mentioned in this article are very good indicators and analysis tools that a terminal operator can use in order to determine the efficiency of its terminal. And also to create a plan in order to improve the market share of the terminal. Nevertheless, besides these six factors there are many other factors that can help to evaluate the competition and were not mentioned in this article.

If you are a terminal operator have you thought about these factors?

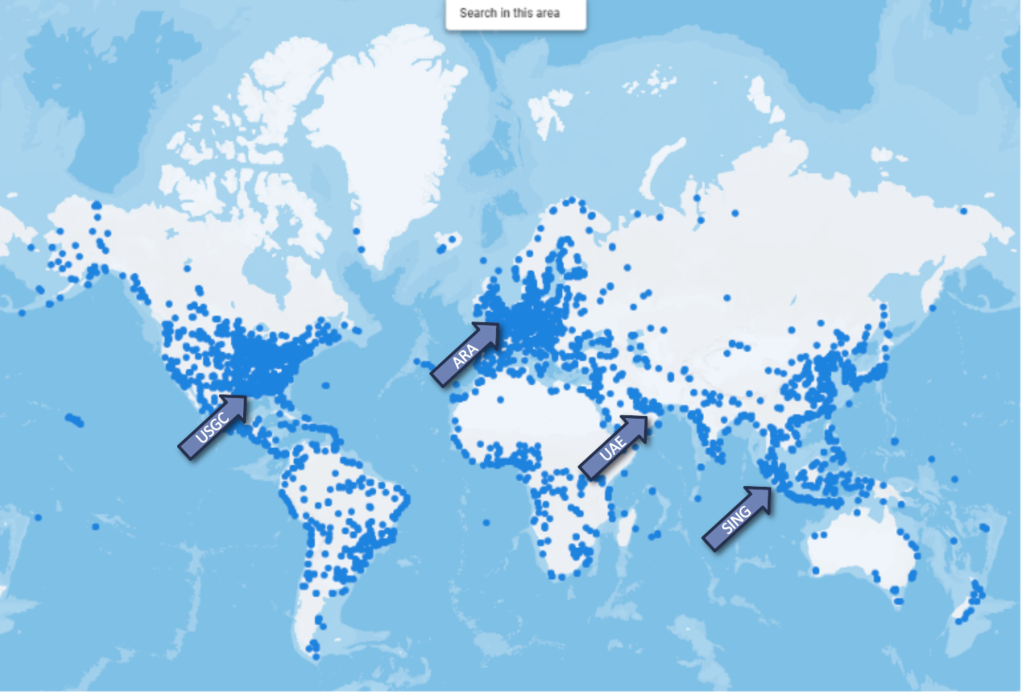

In the world of international tank storage, thousands of terminals give access to commercial storage. These terminals are located all over the world. From large tank farms in oil trading hubs in ARA, USGC, Fujairah and Singapore to small depots on Guam or Greenland.

The tank storage sector is not a static industry but a dynamic one which grows every year. It is interesting to find out which regions have the most investments planned or are currently building new additions.

In picture 1 can be seen where the largest concentrations of tank terminals are.

The world’s hottest storage hotspots

Estimates are that global tank storage capacity will grow 8% to 1.03 billion cbm in 2020 and even 11.5% to 1.06 billion cbm in 2021.

When ranking the regions with the largest total tank capacity in 2019 the following list can be produced: 1) Asia (360Mcbm), 2) Europe (235Mcbm), 3) North America (191Mcbm), 4) Middle East (50.8Mcbm), 5) South America (45.5Mcbm), 6) Africa (43.6Mcbm), and 7) Oceania (4.4Mcbm).

In 2020 the ranking is as followed: 1) Asia (383.7Mcbm), 2) Europe (244Mcbm), 3) North America (207Mcbm), 4) Middle East (93.3Mcbm), 5) Africa (48.9Mcbm), 6) South America (47.8Mcbm), and 7) Oceania (4.7Mcbm).

Analyzing this list some remarkable conclusion can be taken:

-The Middle East will show the strongest growth rate with 84% in 2020 as capacity in this regions grows from 50.8Mcbm to 93.3Mcbm;

-Africa will leapfrog South America and take position 5. This continent shows a growth rate of 12%. Storage capacity increases from 43.6Mcbm to 48.9Mcbm.

-Europe will grow by 4% till 2020 and is the slowest growing region of all the 7 regions. Capacity in this region grows from 235Mcb to 244Mcbm

Although, looking at regions is sort of looking at it as from a macro-level perspective, we can well say that the Middle East will be the hottest tank terminal location in 2020. There are some interesting locations in the Middle East that have a substantial part in the additions in this region.

Fast growing areas in the Middle East

Oman Tank Terminal in Raz Markaz

In Oman storage of oil liquids is concentrated around the ports of Salalah, around Oman’s capital Muscat and Sohar’s industrial area. Oman’s government owned investment company OOC, Oman Oil Company announced a major investment in 2012 on building a massive 31Mcbm crude storage facility in Ras Markaz. Some 200 tanks will be added. Estimates are that this terminal will be operational as from June 2019. With this investment Oman is trying to develop its position as an important global trading and storage hub.

South Oil Company in Iraq

Roughly said, Iraq has storage facilities in its oil fields in the North, around Kirkuk, Al Anbar and Erbil and in the South, around Basrah. Most of these terminals are controlled by the Ministry of Oil of the Republic of Iraq. Government-owned South Oil Company will add 2.78Mcbm of crude capacity in Al Zubair and another 0.464Mcbm in Fao. For the first addition applies that some 489 crude tanks will be built. December 2019 has been pointed as data of operation. For the latter, applies that 5 tanks will be built and this expansion is planned to become operational in December 2020.

Jask Oil Terminal in Iran

In Iran, storage facilities are controlled by state-owned Iranian Oil Terminals CO. These terminals are mostly located at the Persian Gulf and the gulf of Oman, connected with each-other by the infamous Strait of Hormuz. Not in the 2019 and 2020 numbers but definitely worth mentioning is the 10Mcbm crude addition in Jask. Jask is peninsula that runs into the Gulf of Oman. The Jask Oil Terminal will include 20 tanks with floating roofs. he terminal will also include loading and unloading wharves, offshore facilities including three single-point mooring (SPM), and other infrastructure for import/export oil. Estimates are that this addition will be active in December 2021.

The data for this article was gathered with the support of tankterminals.com’s database platform. With only a few clicks and couple of seconds the information of the biggest market players in the various regions was obtained.

For more information, contact: Jacob van den Berge, Head of Marketing & Sales Insights Global

In the global commercial tank storage industry thousands of terminal operators are active. Without taking a terminal operator’s specific function, it is interesting to learn who the biggest players are in the international tank terminal industry.

In picture 1 can be seen where the largest concentrations of tank terminals are.

Looking on a global level the following top 10 terminal operators can be derived. See table 1.

Rank

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Head office

Sinopec

Vopak

CNPC

Kinder Morgan

PetroChina

Buckeye

Oiltanking

Marathon

Enterprise

Magellan

# of terminals

51

69

24

96

34

114

73

99

55

93

Capacity

44.1Mcbm

33.1Mcbm

25.7Mcbm

21.7Mcbm

19.8Mcbm

18.1Mcbm

17.6Mcbm

16.7Mcbm

13.2Mcbm

13.1Mcbm

As can be seen in this list, based on total capacity, the biggest players are located in China with Sinopec, CNPC and PetroChina, followed by US with Kinder Morgan, Buckeye, Marathon, Enterprise and Magellan and Europe with Vopak and Oiltanking. With a combined total capacity of 223Mcbm, the top 10 players cover around 21% of the total capacity globally.

A bit more details on the three biggest storage operators

Sinopec Group, Chinese dragon at the top of the food chain

Sinopec Group, China Petroleum and Chemical Corporation, is a Chinese energy company based in Beijing (China). It is the second largest oil producing company after PetroChina. Besides 50 terminals (with a total storage capacity of 44Mcbm, mostly located in China) and 30.000 petrol stations, this company operates dozens of refineries, around half of the Chinese refinery capacity. Sinopec has various listings on stocks exchanges but for the majority the shares remains in the hands of the Chinese government. In 2017, total revenues was around €300 billion.

Vopak, Dutch giant with a global storage print

Vopak is an independent storage player with a long history dating back to the early 16the century. Independent means it does not own the oil products its stores. It therefor holds an independent position in the market unlike for instance Sinopec and CNPC, the number 1 and 3 in the list. The 69 terminals of Vopak are scattered around the globe. It has locations in more than 20 countries with largest concentration of terminals in the Netherlands, followed by China and the US. In 2018, Vopak’s revenues lay at €1.25 billion.

China National Petroleum Corp, a powerful energy emperor

CNPC is a one of the biggest vertical integrated oil companies in the world. Its origins date back to 1949 when communist China was formed. The company rose from Ministry of Petroleum which secured and managed the country’s fuel. It operates oil assets in more than 30 countries, except for the 24 storage terminals (with a total capacity of 25.7Mcbm) which are mainly located in the Chinese homeland. In the downstream area it also operates more than 20.000 petrol stations.

Are storage capacity market shares equal across the globe’s regions?

Is the global division of market shares similar for the different regions? Absolutely not. Let us analyze the regions with the largest concentration of terminals. The regions with the most terminals are the United States (1.447), Europe (1,125) and Asia (1.057).

In the United States, the tank storage is dominated by publicly owned storage operators with US origins. The top three consist of 1) Kinder Morgan, 2) Magellan and 3) Buckeye. The remainder of the top 10 consists only out of US-born tank storage players.

In Europe, the top 3 biggest players are 1) Vopak, 2) Oiltanking and 3) CLH. These companies are also publicly owned and have a broad international coverage which means they have a global storage footprint. For instance Vopak is ranked number 6 in Asia and Oiltanking is ranked number 12 in Asia.

In Asia the top 3 consist solely of Chinese state-owned companies: 1) Sinopec, 2) CNPC and 3) PetroChina. Their number four is a Japanese company, JX Nippon Corporation and the number five as the Korean Gas Corporation. As mentioned before, ranked six is Vopak.

As can be concluded, the global players take a large piece of the pie. However, there is enough room for other tank terminal players to operate a sustainable business in specific regions, countries or ports. Furthermore, the competitive dynamics differ per region, so tank terminal players face different opponents in various regions.

The data for this article was gathered with the support of TankTerminals.com’s database platform. With only a few clicks and couple of seconds the information of the biggest market players in the various regions was obtained.

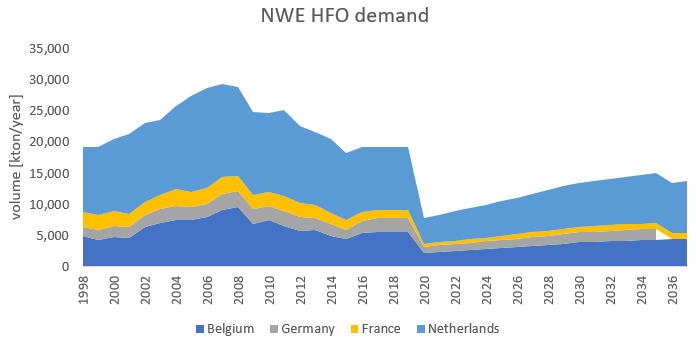

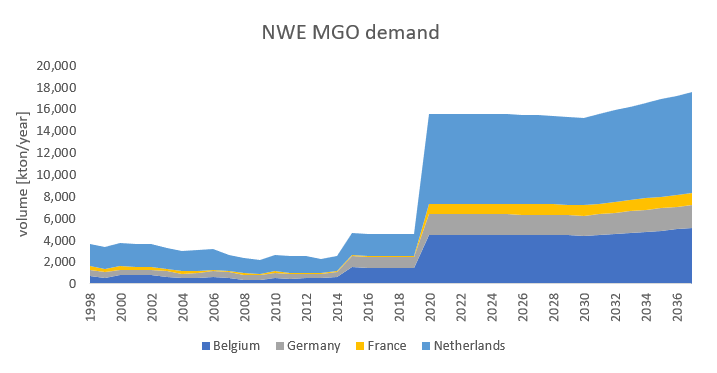

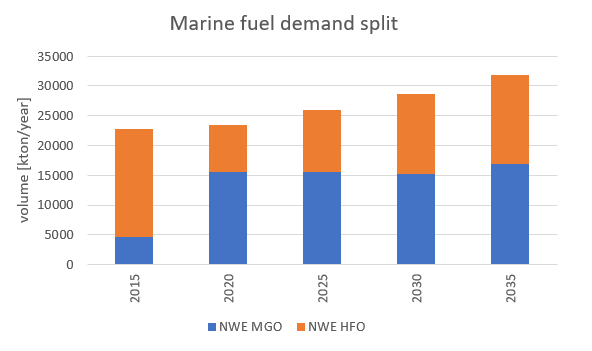

Insights Global structurally forecasts the future supply and demand of oil products in the ARA region and naturally incorporates IMO 2020 into its models. In our forecasting models we predict an annual growth rate for marine fuels that is adjusted for efficiency gains of ships, while the split between HSFO and MGO in bunker demand switches in 2020 and is submissive to price changes and upcoming alternative fuels. We predict a sharp decline in heavy fuel oil demand with simultaneously a jump in the demand for (marine) gasoil in 2020. The heavy fuel oil demand is expected to more than half in size, whereas MGO demand is predicted to quadruple. Our assumption for the post-2020 era is that the shipping industry will gradually switch back to fuel oil using scrubbers or 0.5% LSFO. Furthermore, LNG will take in a more dominant position, up to 11% in 2030. This will diminish the share of gasoil used and lead to a slight decline in gasoil demand between 2020 and 2030.

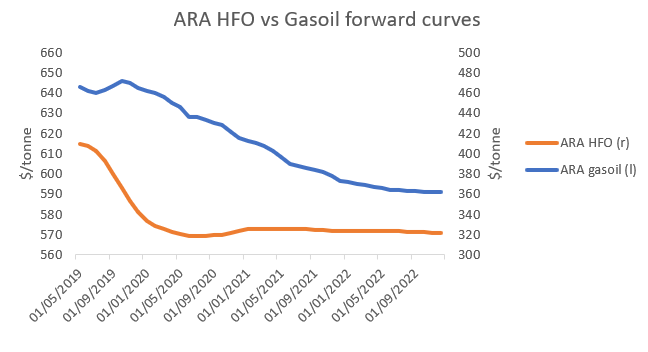

The transition from high sulphur fuel oil to marine gasoil and the changing demands for both products can be seen in the futures markets. The forward curve for HFO makes a steep dive towards the beginning of 2020 when the regulation comes into force. The gasoil prices show an inverted pattern: a small contango until the start of 2020 can be seen as demand for the product will be the largest when the legislation becomes active. After these initial price extremities of gasoil and HFO the markets settle down as HFO prices recover slightly while gasoil prices enter a backwardated situation. This is in line with our demand forecasts and resembles the extent to which alternatives such as scrubbers gain an increasingly larger share. We expect subsequent waves of investments in shipping but also in refining, as the production of 0.5% fuel oil becomes more profitable. For more complex refineries with a certain crude slate this will offer opportunities while for other, more simply configured refineries, their continuity is at stake.

A Change for

the Tank Storage Business

The ARA region currently is a

net-importer of gasoil and is the final destination for many of the world’s

gasoil flows. Estimates are that in 2022 the deficit would increase by between

+12% and +34% relative to 2018 values, primarily driven by IMO 2020. The changing imbalances of gasoil

and fuel oil in the ARA region will have an impact on the ARA tank storage

business. The lower fuel oil demand will increase the oversupply of fuel oil in

the region and as such affect all tank terminals who lend their facility to

this product. The

changing environment for fuel oil tank storage will eventually lead to higher fuel

oil storage rates in the region. Fuel oil storage rates are likely to remain depressed in

2019, but when the IMO regulation hits the markets in 2020 the oversupply of fuel oil is likely

to switch the markets into a contango, supporting the storage business. This

effect is expected to be reinforced when the crude markets switch to contango

as well.

Higher storage rates for fuel oil

are thus expected, but the current fuel oil tank storage business nevertheless faces

a tough time from a logistical point of view. Terminals in ARA specialized in fuel oil are

either busy in the bunkering market or in the transit business. In the first

case these terminals will suffer from the reduced size of the HFO bunker

market. In the second case the business is more related to the flow from Russia

towards Far-East. This transit flow is also expected to be marginalized in the

medium term and long term. Therefore tank terminal operators storing HFO will

need to anticipate on these changes and explore options in order to cope with

possible oversupply of fuel oil tanks. Less tanks for fuel oil storage will be

needed, but opportunities lie in diversification. From 2020 onwards more grades

of bunker fuel (a.o. ULSFO, 0.5% LSFO, 3.5% HSFO) will need to be stored, while

smaller tanks as well as blending capabilities will become more important.

Running up to the bunker fuel spec

change in 2020 the fundamentals for the gasoil storage market are likely to

improve following more interest in middle distillate tanks and the need for

more grades of gasoil. The contango that is developing in the gasoil markets

supports the storage rates as well. In 2020 however we expect a halt to the

growth of gasoil storage rates caused by a backwardated market structure

following the higher spot prices. After 2020 we expect storage rates to improve

with the gasoil markets following the contango formation in the crude markets,

albeit to a smaller extent. More tanks are needed in this bunker market to

store middle distillates which could increase competition, but occupancy rates

in the medium term will remain high due to increased demand.

In 2020 the international marine bunker fuel markets are in for a big change. For environmental concerns the International Maritime Organization will implement a new policy that limits the sulphur content of fuels burnt in maritime traffic. High sulphur fuel oil has been historically the most widely used fuel for maritime transport, but will most likely lose this position to low sulphur fuels such as marine gasoil or LSFO when the new regulation comes into force. This article dives deeper into the subject, and shares our vision on how the ARA bunkering market and international oil markets will change under the new policy.

As of January 1st 2020 the International Maritime Organization (IMO) requires all marine fuels to have a sulphur content of at most 0.5% of the total mass, down from the current maximum allowed 3.5%. With the exception of a few areas that already have special IMO requirements in place, the new IMO standard will hold globally. Traditionally the bunker fuel market has been a sink for refiners to unload their high sulphur refining resids into. In 2018 an average of seven million barrels of such heavy resids were produced every day, half of which was absorbed by ship bunkers. But the global refining system is not yet equipped to produce such quantities of fuel oil at a sulphur level of 0.5%. The impact of this new regulation is therefore big as most vessels will have to abandon their current fuel oil consumption, therewith completely changing the market dynamics for existing marine fuels and creating opportunities for alternatives.

An important decision for shipowners

The shipping industry faces an important decision for their fuel use under the IMO 2020 regulation, and several options exist for shipowners who need to replace their HSFO consumption.

The most likely scenario is that the majority of the shipping industry switches to using marine gasoil (MGO), which doesn’t require any technical modifications nor upfront investments.

Second, the shipping industry could switch to a new 0.5% low sulphur fuel oil (LSFO) grade. Current global LSFO production capacity is however insufficient to cover a transition from HSFO to LSFO in the bunkering industry, and this change would need vast refinery investments.

The third option is to install scrubbers on board of ships and continue to burn HSFO while the exhaust gasses are being filtered. This is an expensive and lengthy investment for the shipowner, as installation costs range between 2-3 million per vessel and the delivery time to install the scrubber will have the vessel out of operation for a long time.

The fourth option is that the shipping industry switches to burning LNG. Significant investments and concerns about the availability of LNG as a bunker fuel however challenge the implementation.

The fifth option is that the shipping industry switches to methanol. Methanol has a low energy density however and in addition requires a multi-million investment. Given the ease of the transition to marine gasoil compared to the other products the market will initially shift its bunker demand by using marine gasoil when the new regulation goes into effect.