As one of the most crucial tank storage hubs in the world, Singapore and nowadays the greater Singapore region play a fundamental role in global trade.

Far East and the ISC countries have experienced tremendous economic growth over the past decades, and this upward trend even has had an impulse after the global financial crisis in 2008. Going forward, trade imbalances, regulations and newly build capacity will continue to influence opportunities in the tank terminal industry in the greater Singapore region.

REGIONAL DEMAND FOR OIL PRODUCTS REMAINS STRONG

The continuously growing economies have driven supply and demand for oil products in Asia, with the Indian and especially Chinese economy increasing their production substantially. China, India, Japan and South Korea are the region’s largest suppliers of oil products, with China more than doubling any other country’s output in 2017.

Far East and the ISC refinery output primarily consists of diesel and gasoline, accounting for 44% and 26% of the region’s total output in 2017 respectively. The productions of both products grew rapid over the past decade, more than any other main refinery output, while demand for both products in the region has increased gradually over the last decade.

Far East and the ISC has surplussus of diesel, gasoline and jet-kerosene, meaning it produces more than it consumes of these products. A higher surpluss generally leads to higher exports of a product, implying an increased demand for temporary tank storage capacity. Deficits exist for fuel oil, naphtha and LPG, meaning Far East and the ISC has to import these products from outside of the region. Singapore’s tank terminal industry has been benefiting from this situation for a long time.

SINGAPORE ON ALERT AS NEIGHBORS’ TANK STORAGE MARKET SHARE INCREASES

Malaysia and Indonesia aim at increasing their market share both approaching Singapore’ total tank storage capacity, while Singapore stays on alert with only minor expansions.

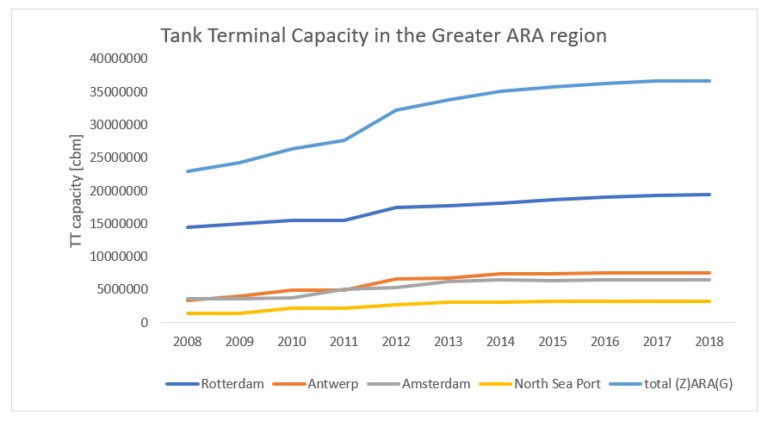

Singapore has been the largest provider of tank capacity in the Greater Singapore area and has roughly tripled its capacity since 2005, especially during the prolonged period of contango between 2005 and 2011, which supported demand for tank capacity. Market circumstances were less favorable after 2011, but the construction of new capacity had already begun adding new storage tanks after this date.

Malaysia is expected to almost double its capacity in 2018 with 4,900,000m3, while in Singapore a total of 370,000 m3 or a mere 2% of its total capacity is being constructed as of 2018. Indonesia has no capacity that is noteworthy under construction but has plans to add more than 7 million m3 in the future. This expansion would more than double the country’s total capacity, but whether these plans will be executed is uncertain.

Singapore will therefore primarily see increased competition from Malaysian tank storage operators.

PREPARING FOR A NEW SET OF CHALLENGES

The Tank Terminal industry in the Greater Singapore area is facing some new challenges, such as new restrictions on emissions, IMO 2020’s new bunker fuel specifications and logistical developments in Asia.

Environmental regulations will have a downforce to gasoline and diesel demand in the region, changing national imbalances and thus trade flows. A sharp decline in fuel oil demand as of 2020 on the other hand, will increase marine gasoil demand, which will result in less temporary storage of fuel oil in Singapore and increase the demand for temporary storage of marine gasoil.

There may also be pressure on demand for marine bunkering and temporary oil products storage in Singapore when alternative cargo routes replace the Strait of Malacca. These could include new One Belt One Road trade routes and China’s two Ocean’s strategy via pipelines through Myanmar.

Click here to read Part 2 of the article “Greater Singapore Tank Storage Market Outlook 2018”.

SINGAPORE TANK TERMINAL MARKET STUDY 2018

Based on extensive market research, Insights Global – in partnership with Ener8 Limited – has produced a +75 pages report providing insights into the Tank Terminal Market in both Singapore and the greater Singapore area.

Click here to download the table of contents.

For more information on how to purchase this report please contact info@insights-global.com