INTRODUCTION

This is the second blog article of our series of 5 blog articles made for you to be able to better understand the drivers and the complexity of the tank storage industry. In the first article we took a closer look at the functions of a tank terminal.

HOW DO TRADERS MAKE MONEY?

Traders can take a physical (&paper) position and ‘buy low / sell high’ to be able to make profit. There are several strategies to profit from trading physical commodities. We can distinguish three main strategies:

| 1. | Arbitrage |

| 2. | Speculation |

| 3. | Optionality |

ARBITRAGE

Arbitrage is a very simple idea, it is really taking advantage in the difference of price on essentially the same product, to make profit. For example if you would have the price of gasoline in two different geographical markets. These different markets can be the Netherlands (A) and the US (B). If in market A the price would 1 dollar and in market B the price would be 2 dollars, then you can profit from the difference in price. The three main types of arbitrage are:

| 1. | Geographical arbitrage |

| 2. | Time arbitrage |

| 3. | Technical arbitrage (blending) |

SPECULATION

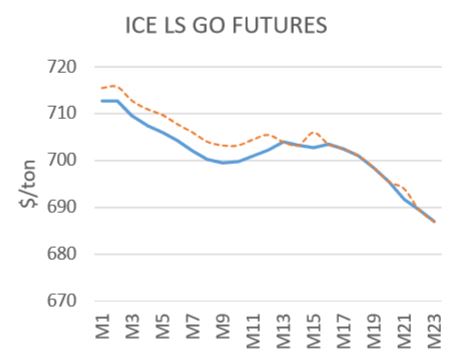

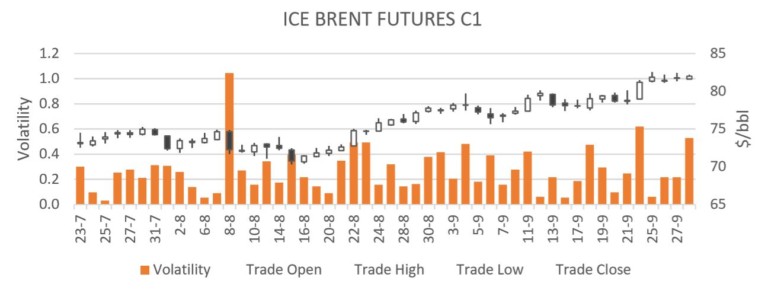

The U.S. Commodities Future Trading Commission defines a speculator as a trader who does not hedge, but who trades with the objective of achieving profits through the successful anticipation of price movements. Traders take a position in anticipation of moves in prices/spreads. For example with the gasoil price as is shown in the chart below:

OPTIONALITY

As for speculation, also for optionality volatility is key. Profit can come from market opportunities, where traders can limit losses if market turns against position. Three examples are:

- Optionality during geographic arbitrage trade. For example divert ship if there is a better deal and reduce costs

- Optionality during contango storage. Contango means that the spot price of oil is lower than future contract for oil

- Optionality in transport mode. Can be applied when transport costs are market driven and volatile

CONCLUSION

More familiarity within this complex market can provide you with quick insights derived from the financial markets. By watching and following oil prices spreads and market volatility can provide you with a better picture of the market. Other trends like backwardation and contango are also important to understand and analyse, to be able to make intelligent decisions. More to come in the next blog article next week, meanwhile feel free to download last week’s tank terminal report. And try to test your comprehension of the subjects discussed.

For more information or any questions please do not hesitate to contact us.